Berkshire Hathaway 2014 Annual Report Download - page 12

Download and view the complete annual report

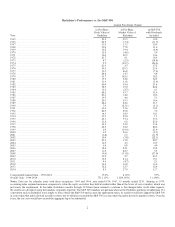

Please find page 12 of the 2014 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Indeed, we are far more conservative in avoiding risk than most large insurers. For example, if the

insurance industry should experience a $250 billion loss from some mega-catastrophe – a loss about triple anything

it has ever experienced – Berkshire as a whole would likely record a significant profit for the year because of its

many streams of earnings. We would also remain awash in cash and be looking for large opportunities in a market

that might well have gone into shock. Meanwhile, other major insurers and reinsurers would be far in the red, if not

facing insolvency.

Ajit’s underwriting skills are unmatched. His mind, moreover, is an idea factory that is always looking

for more lines of business he can add to his current assortment. Last year I told you about his formation of Berkshire

Hathaway Specialty Insurance (“BHSI”). This initiative took us into commercial insurance, where we were instantly

welcomed by both major insurance brokers and corporate risk managers throughout America. Previously, we had

written only a few specialized lines of commercial insurance.

BHSI is led by Peter Eastwood, an experienced underwriter who is widely respected in the insurance

world. During 2014, Peter expanded his talented group, moving into both international business and new lines of

insurance. We repeat last year’s prediction that BHSI will be a major asset for Berkshire, one that will generate

volume in the billions within a few years.

************

We have another reinsurance powerhouse in General Re, managed by Tad Montross.

At bottom, a sound insurance operation needs to adhere to four disciplines. It must (1) understand all

exposures that might cause a policy to incur losses; (2) conservatively assess the likelihood of any exposure actually

causing a loss and the probable cost if it does; (3) set a premium that, on average, will deliver a profit after both

prospective loss costs and operating expenses are covered; and (4) be willing to walk away if the appropriate

premium can’t be obtained.

Many insurers pass the first three tests and flunk the fourth. They simply can’t turn their back on business

that is being eagerly written by their competitors. That old line, “The other guy is doing it, so we must as well,”

spells trouble in any business, but in none more so than insurance.

Tad has observed all four of the insurance commandments, and it shows in his results. General Re’s huge

float has been considerably better than cost-free under his leadership, and we expect that, on average, to continue.

We are particularly enthusiastic about General Re’s international life reinsurance business, which has grown

consistently and profitably since we acquired the company in 1998.

It can be remembered that soon after we purchased General Re, it was beset by problems that caused

commentators – and me as well, briefly – to believe I had made a huge mistake. That day is long gone. General Re

is now a gem.

************

Finally, there is GEICO, the insurer on which I cut my teeth 64 years ago. GEICO is managed by Tony

Nicely, who joined the company at 18 and completed 53 years of service in 2014. Tony became CEO in 1993, and

since then the company has been flying. There is no better manager than Tony.

When I was first introduced to GEICO in January 1951, I was blown away by the huge cost advantage the

company enjoyed compared to the expenses borne by the giants of the industry. It was clear to me that GEICO

would succeed because it deserved to succeed. No one likes to buy auto insurance. Almost everyone, though, likes

to drive. The insurance consequently needed is a major expenditure for most families. Savings matter to them – and

only a low-cost operation can deliver these. Indeed, at least 40% of the people reading this letter can save money by

insuring with GEICO. So stop reading and go to geico.com or call 800-368-2734.

10