APS 2011 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2011 APS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

70

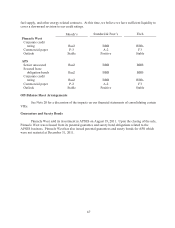

(a) Each fluctuation assumes that the other assumptions of the calculation are held constant while

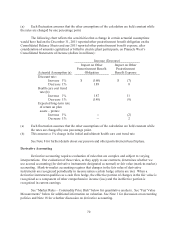

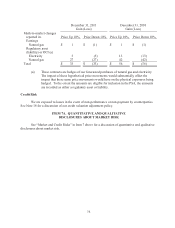

the rates are changed by one percentage point.

The following chart reflects the sensitivities that a change in certain actuarial assumptions

would have had on the December 31, 2011 reported other postretirement benefit obligation on the

Consolidated Balance Sheets and our 2011 reported other postretirement benefit expense, after

consideration of amounts capitalized or billed to electric plant participants, on Pinnacle West’s

Consolidated Statements of Income (dollars in millions):

Increase (Decrease)

Actuarial Assumption (a)

Impact on Other

Postretirement Benefit

Obligation

Impact on Other

Postretirement

Benefit Expense

Discount rate:

Increase 1% $ (160) $ (7)

Decrease 1% 189 8

Health care cost trend

rate (b):

Increase 1% 187 11

Decrease 1% (148) (9)

Expected long-term rate

of return on plan

assets – pretax:

Increase 1% -- (2)

Decrease 1% -- 2

(a) Each fluctuation assumes that the other assumptions of the calculation are held constant while

the rates are changed by one percentage point.

(b) This assumes a 1% change in the initial and ultimate health care cost trend rate.

See Note 8 for further details about our pension and other postretirement benefit plans.

Derivative Accounting

Derivative accounting requires evaluation of rules that are complex and subject to varying

interpretations. Our evaluation of these rules, as they apply to our contracts, determines whether we

use accrual accounting (for derivative instruments designated as normal) or fair value (mark-to-market)

accounting. Mark-to-market accounting requires that changes in the fair value of derivative

instruments are recognized periodically in income unless certain hedge criteria are met. When a

derivative instrument qualifies as a cash flow hedge, the effective portion of changes in the fair value is

recognized as a component of other comprehensive income (loss) and the ineffective portion is

recognized in current earnings.

See “Market Risks – Commodity Price Risk” below for quantitative analysis. See “Fair Value

Measurements” below for additional information on valuation. See Note 1 for discussion on accounting

policies and Note 18 for a further discussion on derivative accounting.