The Hartford 2013 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2013 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

34

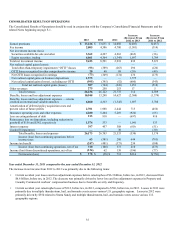

THE HARTFORD’S OPERATIONS OVERVIEW

The Hartford is a financial holding company for a group of subsidiaries that provide property and casualty and investment products to

both individual and business customers in the United States and continues to administer life and annuity products previously sold.

On January 1, 2013, the Company completed the sale of its Retirement Plans business to Massachusetts Mutual Life Insurance Company

("MassMutual") and on January 2, 2013 the Company completed the sale of its Individual Life insurance business to The Prudential

Insurance Company of America ("Prudential"), a subsidiary of Prudential Financial, Inc. On December 12, 2013, the Company

completed the sale of Hartford Life International Limited ("HLIL"), which comprised the Company's U.K. variable annuity business, to

Columbia Insurance Company, a Berkshire Hathaway company. For further discussion of these and other such transactions, see Note 2 -

Business Dispositions, Note 7 - Reinsurance and Note 20 - Discontinued Operations of Notes to Consolidated Financial Statements.

The Company derives its revenues principally from: (a) premiums earned for insurance coverages provided to insureds; (b) fee income,

including asset management fees, on separate account and mutual fund assets and mortality and expense fees, as well as cost of

insurance charges; (c) net investment income; (d) fees earned for services provided to third parties; and (e) net realized capital gains and

losses. Premiums charged for insurance coverages are earned principally on a pro rata basis over the terms of the related policies in-

force. Asset management fees and mortality and expense fees are primarily generated from separate account assets. Cost of insurance

charges are assessed on the net amount at risk for investment-oriented life insurance products.

The profitability of the Company's property and casualty insurance businesses over time is greatly influenced by the Company’s

underwriting discipline, which seeks to manage exposure to loss through favorable risk selection and diversification, its management of

claims, its use of reinsurance, the size of its in force block, actual mortality and morbidity experience, and its ability to manage its

expense ratio which it accomplishes through economies of scale and its management of acquisition costs and other underwriting

expenses. Pricing adequacy depends on a number of factors, including the ability to obtain regulatory approval for rate changes, proper

evaluation of underwriting risks, the ability to project future loss cost frequency and severity based on historical loss experience adjusted

for known trends, the Company’s response to rate actions taken by competitors, and expectations about regulatory and legal

developments and expense levels. The Company seeks to price its insurance policies such that insurance premiums and future net

investment income earned on premiums received will cover underwriting expenses and the ultimate cost of paying claims reported on

the policies and provide for a profit margin. For many of its insurance products, the Company is required to obtain approval for its

premium rates from state insurance departments.

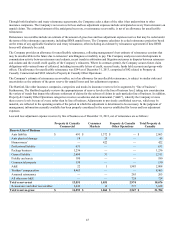

The financial results in the Company’s variable annuity and mutual fund businesses depend largely on the amount of the contract holder

or shareholder account value or assets under management on which it earns fees and the level of fees charged. Changes in account value

or assets under management are driven by two main factors: net flows, which measure the success of the Company’s asset gathering and

retention efforts, and the market return of the funds, which is heavily influenced by the return realized in the equity markets. Net flows

are comprised of deposits less surrenders, death benefits, policy charges and annuitizations of investment type contracts, such as variable

annuity contracts. In the mutual fund business, net flows are known as net sales. Net sales are comprised of new sales less redemptions

by mutual fund customers. The Company uses the average daily value of the S&P 500 Index as an indicator for evaluating market

returns of the underlying account portfolios in the United States. Relative financial results of variable products are highly correlated to

the growth in account values or assets under management since these products generally earn fee income on a daily basis. Equity market

movements could also result in benefits for or charges against deferred acquisition costs.

The profitability of fixed annuities and other “spread-based” products depends largely on the Company’s ability to earn target spreads

between earned investment rates on its general account assets and interest credited to policyholders. In addition, the size and persistency

of gross profits from these businesses is an important driver of earnings as it affects the rate of amortization of deferred policy

acquisition costs.

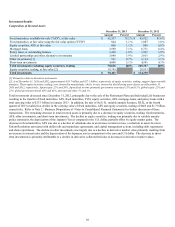

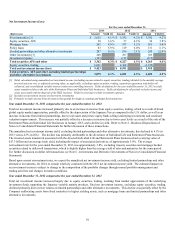

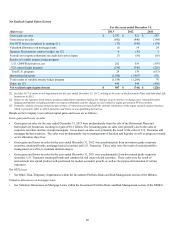

The investment return, or yield, on invested assets is an important element of the Company’s earnings since insurance products are

priced with the assumption that premiums received can be invested for a period of time before benefits, loss and loss adjustment

expenses are paid. Due to the need to maintain sufficient liquidity to satisfy claim obligations, the majority of the Company’s invested

assets have been held in available-for-sale securities, including, among other asset classes, corporate bonds, municipal bonds,

government debt, short-term debt, mortgage-backed securities and asset-backed securities.

The primary investment objective for the Company is to maximize economic value, consistent with acceptable risk parameters, including

the management of credit risk and interest rate sensitivity of invested assets, while generating sufficient after-tax income to meet

policyholder and corporate obligations. Investment strategies are developed based on a variety of factors including business needs,

regulatory requirements and tax considerations.