The Hartford 2013 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2013 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

125

Liquidity requirements that are unable to be funded by Property & Casualty Operation’s short-term investments would be satisfied with

current operating funds, including premiums received or through the sale of invested assets. A sale of invested assets could result in

realized losses.

Life Operations

Life Operations’ total general account contractholder obligations are supported by $49 billion of cash and total general account invested

assets, excluding equity securities, trading, which includes a significant short-term investment position to meet liquidity needs.

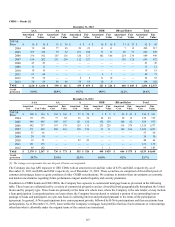

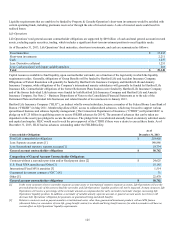

As of December 31, 2013, Life Operations’ fixed maturities, short-term investments, and cash are summarized as follows:

Fixed maturities $ 37,432

Short-term investments 2,211

Cash 1,237

Less: Derivative collateral 1,251

Less: Cash associated with Japan variable annuities 281

Total $ 39,348

Capital resources available to fund liquidity, upon contractholder surrender, are a function of the legal entity in which the liquidity

requirement resides. Generally, obligations of Group Benefits will be funded by Hartford Life and Accident Insurance Company.

Obligations of Talcott Resolution will generally be funded by Hartford Life Insurance Company and Hartford Life and Annuity

Insurance Company, while obligations of the Company’s international annuity subsidiaries will generally be funded by Hartford Life

Insurance KK. Contractholder obligations of the former Retirement Plans business were funded by Hartford Life Insurance Company

and of the former Individual Life business were funded by both Hartford Life Insurance Company and Hartford Life and Annuity

Insurance Company. See Note 2 - Business Dispositions of Notes to the Consolidated Financial Statements as to the sale of the

Retirement Plans and Individual Life businesses and related transfer of invested assets in January 2013.

Hartford Life Insurance Company (“HLIC”), an indirect wholly owned subsidiary, became a member of the Federal Home Loan Bank of

Boston (“FHLBB”) in May 2011. Membership allows HLIC access to collateralized advances, which may be used to support various

spread-based business and enhance liquidity management. [The Connecticut Department of Insurance (“CTDOI”) will permit HLIC to

pledge up to $1.25 billion in qualifying assets to secure FHLBB advances for 2014]. The amount of advances that can be taken are

dependent on the asset types pledged to secure the advances. The pledge limit is recalculated annually based on statutory admitted assets

and capital and surplus. HLIC would need to seek the prior approval of the CTDOI if there were a desire to exceed these limits. As of

December 31, 2013, HLIC had no advances outstanding under the FHLBB facility.

As of

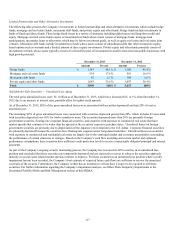

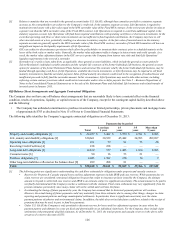

Contractholder Obligations December 31, 2013

Total Life contractholder obligations $ 219,402

Less: Separate account assets [1] 140,886

Less: International statutory separate accounts [1] 19,734

General account contractholder obligations $ 58,782

Composition of General Account Contractholder Obligations

Contracts without a surrender provision and/or fixed payout dates [2] $ 24,625

U.S. Fixed MVA annuities and Other [3] 10,142

International Fixed MVA annuities [3] 1,514

Guaranteed investment contracts (“GIC”) [4] 31

Other [5] 22,470

General account contractholder obligations $ 58,782

[1] In the event customers elect to surrender separate account assets or international statutory separate accounts, Life Operations will use the

proceeds from the sale of the assets to fund the surrender, and Life Operations’ liquidity position will not be impacted. In many instances Life

Operations will receive a percentage of the surrender amount as compensation for early surrender (surrender charge), increasing Life

Operations’ liquidity position. In addition, a surrender of variable annuity separate account or general account assets (see below) will

decrease Life Operations’ obligation for payments on guaranteed living and death benefits.

[2] Relates to contracts such as payout annuities or institutional notes, other than guaranteed investment products with an MVA feature

(discussed below) or surrenders of term life, group benefit contracts or death and living benefit reserves for which surrenders will have no

current effect on Life Operations’ liquidity requirements.