The Hartford 2013 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2013 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

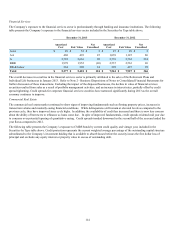

106

Most of these factors are outside of the Company’s control. The Company’s financial strength and credit ratings are significantly

influenced by the statutory surplus amounts and RBC ratios of our insurance company subsidiaries. In addition, rating agencies may

implement changes to their internal models that have the effect of increasing or decreasing the amount of statutory capital we must hold

in order to maintain our current ratings.

The Company has reinsured approximately 20% of its risk associated with U.S. GMWB and 76% of its risk associated with the

aggregate U.S. GMDB exposure. These reinsurance agreements serve to reduce the Company’s exposure to changes in the statutory

reserves and the related capital and RBC ratios associated with changes in the capital markets. The Company also continues to explore

other solutions for mitigating the capital market risk effect on surplus, such as external reinsurance solutions, modifications to our

hedging program, changes in product design, increasing pricing and expense management.

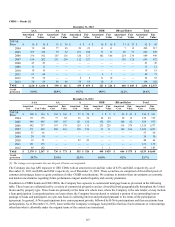

Credit Risk

Credit risk is defined as the risk of financial loss due to uncertainty of an obligor’s or counterparty’s ability or willingness to meet its

obligations in accordance with contractually agreed upon terms. The majority of the Company’s credit risk is concentrated in its

investment holdings but is also present in reinsurance and insurance portfolios. Credit risk is comprised of three major factors: the risk of

change in credit quality, or credit migration risk; the risk of default; and the risk of a change in value of a financial instrument due to

changes in credit spread that are unrelated to changes in obligor credit quality. A decline in creditworthiness is typically associated with

an increase in an investment’s credit spread, potentially resulting in an increase in other-than-temporary impairments and an increased

probability of a realized loss upon sale.

The objective of the Company’s enterprise credit risk management strategy is to identify, quantify, and manage credit risk on an

aggregate portfolio basis and to limit potential losses in accordance with an established credit risk appetite. The Company manages to its

risk appetite by primarily holding a diversified mix of investment grade issuers and counterparties across its investment, reinsurance, and

insurance portfolios. Potential losses are also limited within portfolios by diversifying across geographic regions, asset types, and

sectors.

The Company manages a credit exposure from its inception to its maturity or sale. Both the investment and reinsurance areas have

formulated procedures for counterparty approvals and authorizations. Although approval processes may vary by area and type of credit

risk, approval processes establish minimum levels of creditworthiness and financial stability. Eligible credits are subjected to prudent

and conservative underwriting reviews. Within the investment portfolio, private securities, such as commercial mortgages, and private

placements, must be presented to their respective review committees for approval.

Credit risks are managed on an on-going basis through the use of various processes and analyses. At the investment, reinsurance, and

insurance product levels, fundamental credit analyses are performed at the issuer/counterparty level on a regular basis. To provide a

holistic review within the investment portfolio, fundamental analyses are supported by credit ratings, assigned by nationally recognized

rating agencies or internally assigned, and by quantitative credit analyses. The Company utilizes a credit value at risk ("VaR") to

measure default and migration risk on a monthly basis. Issuer and security level risk measures are also utilized. In the event of

deterioration in credit quality, the Company maintains watch lists of problem counterparties within the investment and reinsurance

portfolios. The watch lists are updated based on regular credit examinations and management reviews. The Company also performs

quarterly assessments of probable expected losses in the investment portfolio. The process is conducted on a sector basis and is intended

to promptly assess and identify potential problems in the portfolio and to recognize necessary impairments.