The Hartford 2013 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2013 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

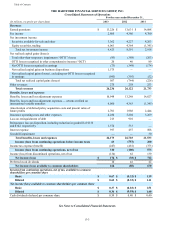

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued)

1. Basis of Presentation and Significant Accounting Policies (continued)

F-9

Mutual Funds

The Company maintains a mutual fund operation whereby the Company provides investment management, administrative and

distribution services to The Hartford-sponsored mutual funds (collectively, “mutual funds”). These mutual funds are registered with the

Securities and Exchange Commission (“SEC”) under the Investment Company Act of 1940. The mutual funds are owned by the

shareholders of those funds and not by the Company. As such, the mutual fund assets and liabilities and related investment returns are

not reflected in the Company’s Consolidated Financial Statements since they are not assets, liabilities and operations of the Company.

Reclassifications

Certain reclassifications have been made to prior year financial information to conform to the current year presentation.

Significant Accounting Policies

The Company’s significant accounting policies are as follows:

Revenue Recognition

Property and casualty insurance premiums are earned on a pro rata basis over the lives of the policies and include accruals for ultimate

premium revenue anticipated under auditable and retrospectively rated policies. Unearned premiums represent the premiums applicable

to the unexpired terms of policies in force. An estimated allowance for doubtful accounts is recorded on the basis of periodic evaluations

of balances due from insureds, management’s experience and current economic conditions. The Company charges off any balances that

are determined to be uncollectible. The allowance for doubtful accounts included in premiums receivable and agents’ balances in the

Consolidated Balance Sheets was $125 and $117 as of December 31, 2013 and 2012, respectively.

Traditional life products premiums are recognized as revenue when due from policyholders. Group life, disability and accident

premiums are generally both due from policyholders and recognized as revenue on a pro rata basis over the period of the contracts.

Fee income for universal life-type contracts consists of policy charges for policy administration, cost of insurance charges and surrender

charges assessed against policyholders’ account balances and are recognized in the period in which services are provided. The amounts

collected from policyholders for investment and universal life-type contracts are considered deposits and are not included in revenue.

Unearned revenue reserves, representing amounts assessed as consideration for policy origination of a universal life-type contract, are

deferred and recognized in income over the period benefited, generally in proportion to estimated gross profits.

The Company provides investment management, administrative and distribution services to mutual funds. The Company charges fees to

these mutual funds which are primarily based on the average daily net asset values of the mutual funds and recorded as fee income in the

period in which the services are provided. Commission fees are based on the sale proceeds and recognized at the time of the transaction.

Transfer agent fees are assessed as a charge per account and recognized as fee income in the period in which the services are provided.

Other revenues primarily consists of servicing revenues which are recognized as services are performed.