Volvo 2009 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2009 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

Notes to consolidated financial statements

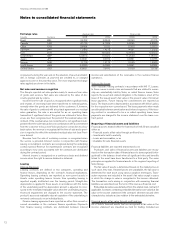

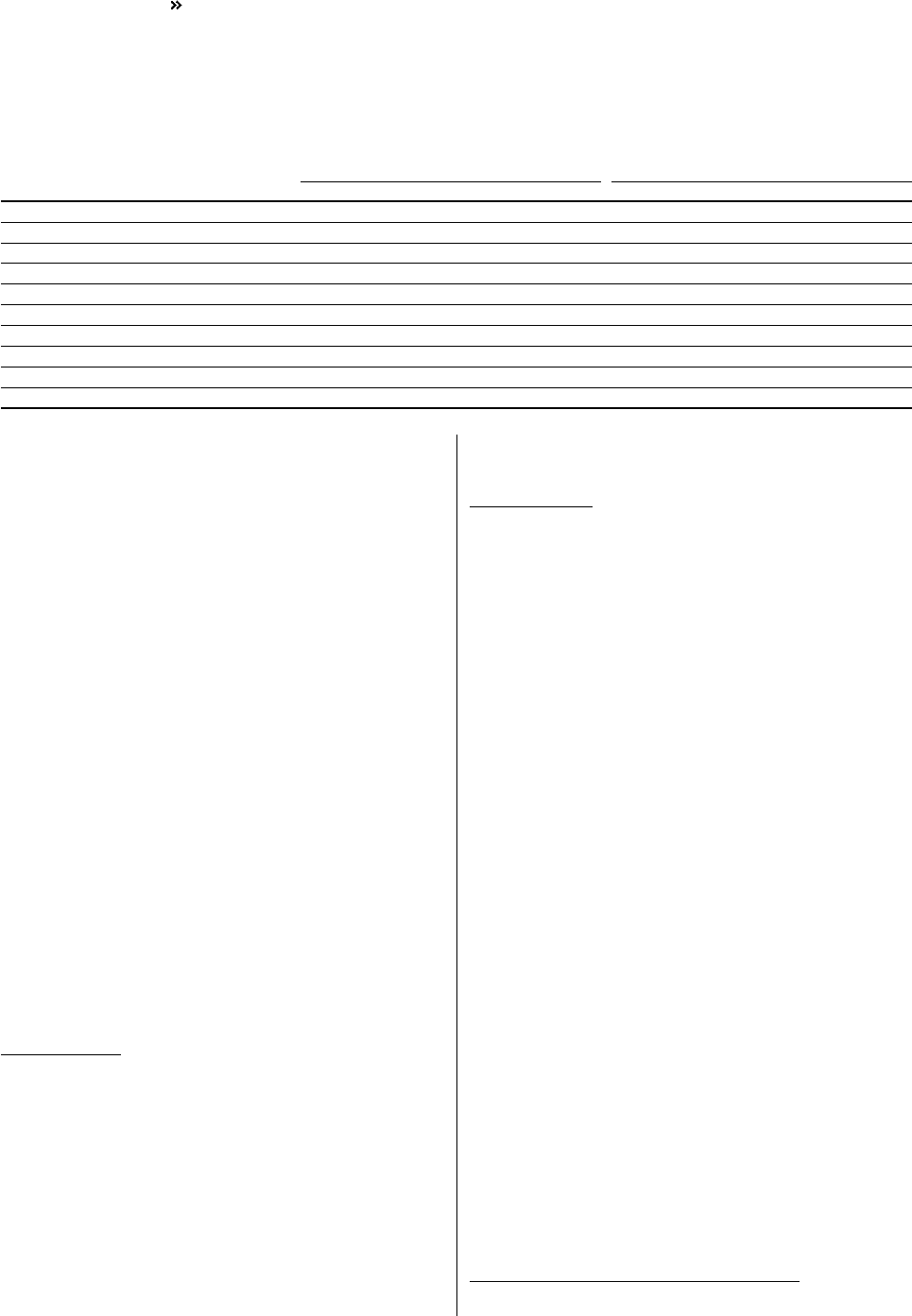

on payments during the year and on the valuation of assets and liabil-

ities in foreign currencies at year-end are credited to, or charged

against, income in the year they arise. The more important exchange

rates applied are shown in the table.

Net sales and revenue recognition

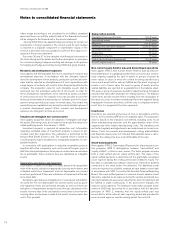

The Group’s reported net sales pertain mainly to revenues from sales

of goods and services. Net sales are reduced by the value of dis-

counts granted and by returns.

Income from the sale of goods is recognized when significant risks

and rewards of ownership have been transferred to external parties,

normally when the goods are delivered to the customers. If, however,

the sale of goods is combined with a buy-back agreement or a residual

value guarantee, the sale is accounted for as an operating lease

transaction if significant risks of the goods are retained in Volvo. Rev-

enues are then recognized over the period of the residual value com-

mitment. If the residual value risk commitment is not significant, inde-

pendent from the sale transaction or in combination with a commitment

from the customer to buy a new Volvo product in connection to a buy-

back option, the revenue is recognized at the time of sale and a provi-

sion is reported to reflect the estimated residual value risk (see Provi-

sions below).

Revenue from the sale of workshop services is recognized when

the service is provided. Interest income in conjunction with finance

leasing or installment contracts are recognized during the underlying

contract period. Revenue for maintenance contracts are recognized

according to how costs associated with the contracts are distributed

during the contract period.

Interest income is recognized on a continuous basis and dividend

income when the right to receive dividend is obtained.

Leasing

Volvo as the lessor

Leasing contracts are defined in two categories, operating and

finance leases, depending on the contract’s financial implications.

Operating leasing contracts are reported as non-current assets in

Assets under operating leases. Income from operating leasing is

reported equally distributed over the leasing period. Straight-line

depreciation is applied to these assets in accordance with the terms

of the undertaking and the deprecation amount is adjusted to corre-

spond to the estimated realizable value when the undertaking expires.

Assessed impairments are charged to the income statement. The

product’s assessed realizable value at expiration of the undertaking is

reviewed continuously on an individual basis.

Finance leasing agreements are reported as either Non-current or

current receivables in the customer finance operations. Payments

from finance leasing contracts are distributed between interest

income and amortization of the receivable in the customer finance

operations.

Volvo as the lessee

Volvo evaluates leasing contracts in accordance with IAS 17, Leases.

In those cases in which risks and rewards that are related to owner-

ship are substantially held by Volvo, so called finance leases, Volvo

reports the asset and related obligation in the balance sheet at the

lower of the leased asset’s fair value or the present value of minimum

lease payments. Future leasing fee commitments are reported as

loans. The lease asset is depreciated in accordance with Volvo’s policy

for the respective non-current asset. The lease payments when made

are allocated between amortization and interest expenses. If the leas-

ing contract is considered to be a so called operating lease, lease

payments are charged to the income statement over the lease con-

tract period.

Reporting of financial assets and liabilities

Financial assets treated within the framework of IAS 39 are classified

either as

– Financial assets at fair value through profit and loss,

– Investments held to maturity,

– Loans and receivables, or as

– Available-for-sale financial assets

Financial liabilities are reported at amortized cost.

Purchases and sales of financial assets and liabilities are recog-

nized on the transaction date. A financial asset is derecognized (extin-

guished) in the balance sheet when all significant risks and benefits

linked to the asset have been transferred to a third party. The same

principles are applied for financial assets in the segment reporting of

Volvo Group.

The fair value of assets is determined based on the market prices in

such cases they exist. If market prices are unavailable, the fair value is

determined for each asset using various valuation techniques. Trans-

action expenses are included in the asset’s fair value except in cases

in which the change in value is recognized in the income statement.

The transaction costs arising in conjunction with assuming financial

liabilities are amortized over the term of the loan as a financial cost.

Embedded derivatives are detached from the related main contract, if

applicable. Contracts containing embedded derivatives are valued at fair

value in the income statement if the contracts’ inherent risk and other

characteristics indicate a close relation to the embedded derivative.

Financial assets at fair value through profit and loss

All of Volvo’s financial assets that are recognized at fair value in the

income statement are classified as held for trading. Included are

Exchange rates Average rate Closing rate

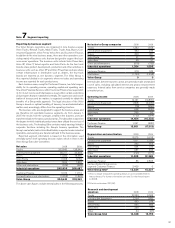

Country Currency 2008 2009 2008 2009

Brazil BRL 3.6152 3.8444 3.2490 4.1375

Canada CAD 6.1723 6.7006 6.3060 6.8885

China CNY 0.9464 1.119 2 1.1300 1.0600

Denmark DKK 1.2895 1.4275 1.4691 1.3926

Euro EUR 9.6142 10.6305 10.9448 10.3623

Great Britain GBP 12.0975 11. 9 32 2 11.2538 11. 4 913

Japan JPY 0.0641 0.0819 0.0861 0.0785

Norway NOK 1.1716 1.2172 1.1045 1.2440

South Korea KRW 0.0060 0.0060 0.0061 0.0062

United States USD 6.5821 7.6470 7.7538 7.2138

FINANCIAL INFORMATION 2009

72