Travelers 2013 Annual Report Download - page 193

Download and view the complete annual report

Please find page 193 of the 2013 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

|

|

THE TRAVELERS COMPANIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

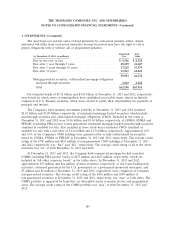

provides 100% of the capital, underwrites through five principal business units—marine, global

property, accident & special risks, power & utilities and aviation.

In addition, the Company owns 49.5% of the common stock of J. Malucelli Participa¸c˜

oes em

Seguros e Resseguros S.A. (JMalucelli), its joint venture in Brazil. JMalucelli is currently the market

leader in surety in Brazil based on market share, and commenced writing other property and casualty

insurance business in 2012. The Company’s investment in JMalucelli is accounted for using the equity

method and is included in ‘‘other investments’’ on the consolidated balance sheet.

Personal Insurance

The Personal Insurance segment writes a broad range of property and casualty insurance covering

individuals’ personal risks. The primary products of automobile and homeowners insurance are

complemented by a broad suite of related coverages.

Automobile policies provide coverage for liability to others for both bodily injury and property

damage, uninsured motorist protection, and for physical damage to an insured’s own vehicle from

collision, fire, flood, hail and theft. In addition, many states require policies to provide first-party

personal injury protection, frequently referred to as no-fault coverage.

Homeowners policies provide protection against losses to dwellings and contents from a variety of

perils (excluding flooding) as well as coverage for personal liability. The Company writes homeowners

insurance for dwellings, condominiums and tenants, and rental properties. The Company also writes

coverage for boats and yachts and valuable personal items such as jewelry, and also writes coverages for

umbrella liability, identity fraud, and weddings and special events.

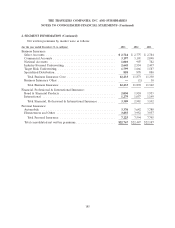

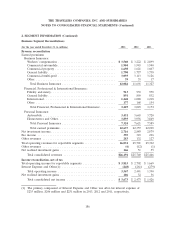

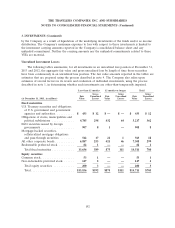

2. SEGMENT INFORMATION

The accounting policies used to prepare the segment reporting data for the Company’s three

reportable business segments are the same as those described in the Summary of Significant Accounting

Policies in note 1.

Except as described below for certain legal entities, the Company allocates its invested assets and

the related net investment income to its reportable business segments. Pretax net investment income is

allocated based upon an investable funds concept, which takes into account liabilities (net of

non-invested assets) and appropriate capital considerations for each segment. For investable funds, a

benchmark investment yield is developed that reflects the estimated duration of the loss reserves’ future

cash flows, the interest rate environment at the time the losses were incurred and A+ rated corporate

debt instrument yields. For capital, a benchmark investment yield is developed that reflects the average

yield on the total investment portfolio. The benchmark investment yields are applied to each segment’s

investable funds and capital, respectively, to produce a total notional investment income by segment.

The Company’s actual net investment income is allocated to each segment in proportion to the

respective segment’s notional investment income to total notional investment income. There are certain

legal entities within the Company that are dedicated to specific reportable business segments. The

invested assets and related net investment income from these legal entities are reported in the

applicable business segment and are not allocated among the other business segments.

The cost of the Company’s catastrophe treaty program is included in the Company’s ceded

premiums and is allocated among reportable business segments based on an estimate of actual market

reinsurance pricing using expected losses calculated by the Company’s catastrophe model, adjusted for

any experience adjustments.

183