Travelers 2013 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2013 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

|

|

In 2013, gross and net Agency written premiums were 5% lower than in 2012. Renewal rate

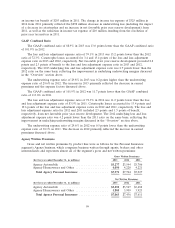

changes continued to exceed expected loss cost trends, assuming weather patterns consistent with the

Company’s expectations. In 2012, gross and net Agency written premiums were 2% lower than in 2011.

In 2013 in the Agency Automobile line of business, net written premiums were 8% lower than in

2012. Business retention rates in 2013 remained strong but were slightly lower than in 2012, while new

business premiums in 2013 decreased from 2012, largely as a result of the Company’s continued pricing

strategies and other profitability improvement initiatives. Renewal premium changes in 2013 remained

positive and were higher than in 2012, primarily driven by renewal rate changes. In 2012, net written

premiums were 4% lower than in 2011. Business retention rates remained strong but were lower than

in 2011, while new business premiums in 2012 decreased from 2011, largely as a result of the

Company’s pricing strategy and other profitability improvement initiatives. Renewal premium changes

remained positive in 2012 and were higher than in 2011.

In 2013 in the Agency Homeowners and Other line of business, net written premiums were 3%

lower than in 2012. Business retention rates remained strong but were slightly lower than in 2012.

Renewal premium changes in 2013 remained positive but were slightly lower than in 2012. New

business premiums in 2013 decreased from 2012. Net written premiums in 2012 were slightly lower than

in 2011. Business retention rates remained strong but were lower than in 2011. New business premiums

in 2012 decreased from 2011, largely as a result of the Company’s pricing strategy, higher deductibles

and other profitability improvement initiatives. Renewal premium changes remained positive in 2012

and were higher than in 2011.

For its Agency business, the Personal Insurance segment had approximately 6.2 million and

6.9 million active policies at December 31, 2013 and 2012, respectively. In the third quarter of 2013, the

Company sold the renewal rights related to its National Flood Insurance Program (NFIP) business.

Active policies in force at both dates have been adjusted to exclude the NFIP business.

Direct to Consumer Written Premiums

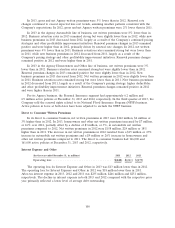

In its direct to consumer business, net written premiums in 2013 were $162 million, $4 million or

3% higher than in 2012. In 2013, homeowners and other net written premiums increased by $7 million,

or 16% over 2012, partially offset by a decline of $3 million, or 3%, in automobile net written

premiums compared to 2012. Net written premiums in 2012 were $158 million, $24 million or 18%

higher than in 2011. The increase in net written premiums in 2012 resulted from a $15 million or 15%

increase in automobile net written premiums and a $9 million or 26% increase in homeowners and

other net written premiums compared to 2011. The direct to consumer business had 166,000 and

161,000 active policies at December 31, 2013 and 2012, respectively.

Interest Expense and Other

(for the year ended December 31, in millions) 2013 2012 2011

Operating loss .................................. $(248) $(261) $(279)

The operating loss for Interest Expense and Other in 2013 was $13 million lower than in 2012.

The operating loss for Interest Expense and Other in 2012 was $18 million lower than in 2011.

After-tax interest expense in 2013, 2012 and 2011 was $235 million, $246 million and $251 million,

respectively. The decline in interest expense in both 2013 and 2012 compared with the respective prior

year primarily reflected a lower level of average debt outstanding.

100