Travelers 2013 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2013 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

|

|

The underwriting expense ratio of 41.1% in 2013 was 0.2 points lower than the underwriting

expense ratio of 41.3% in 2012. The decrease in 2013 primarily reflected the impact of the acquisition

of Dominion, partially offset by the increases in amortization of deferred acquisition costs and general

and administrative expenses described above. Historically, Dominion has had a lower underwriting

expense ratio than the pre-existing business in the Financial, Professional & International Insurance

segment, as the underwriting expense ratio of pre-existing business reflects investment in the

Company’s International business to enhance operations, improve underwriting results and support

future business growth, as well as the business mix in Bond & Financial Products.

The GAAP combined ratio of 84.1% in 2012 was 1.7 points lower than the GAAP combined ratio

of 85.8% in 2011.

The loss and loss adjustment expense ratio of 42.8% in 2012 was 3.6 points lower than the loss and

loss adjustment expense ratio of 46.4% in 2011. The 2012 and 2011 ratios included 9.8 points and 11.3

points of benefit, respectively, from net favorable prior year reserve development. Catastrophe losses in

2012 and 2011 accounted for 1.7 points of the loss and loss adjustment expense ratio in each year. The

2012 underlying loss and loss adjustment expense ratio was 5.1 points lower than the 2011 ratio on the

same basis, reflecting the improvement in underlying underwriting margins discussed in the ‘‘Overview’’

section above.

The underwriting expense ratio of 41.3% in 2012 was 1.9 points higher than the underwriting

expense ratio of 39.4% in 2011, primarily reflecting the impact of a decline in earned premiums and, to

a lesser extent, the impact of an increase in general and administrative expenses.

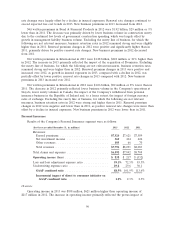

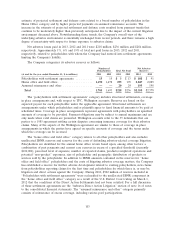

Written Premiums

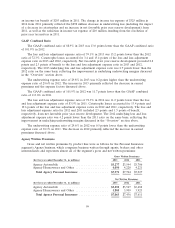

Financial, Professional & International Insurance gross and net written premiums by market were

as follows:

Gross Written Premiums

(for the year ended December 31, in millions) 2013 2012 2011

Bond & Financial Products ....................... $2,131 $2,059 $2,092

International ................................. 1,415 1,216 1,316

Total Financial, Professional & International Insurance $3,546 $3,275 $3,408

Net Written Premiums

(for the year ended December 31, in millions) 2013 2012 2011

Bond & Financial Products ....................... $2,030 $1,924 $1,953

International ................................. 1,279 1,057 1,149

Total Financial, Professional & International Insurance $3,309 $2,981 $3,102

Gross and net written premiums in 2013 increased by 8% and 11%, respectively, over 2012. Gross

and net written premiums in 2012 both decreased by 4% from 2011. Renewal rate changes continued to

exceed expected loss cost trends.

Net written premiums in Bond & Financial Products in 2013 were $2.03 billion, $106 million or

6% higher than in 2012, primarily driven by higher contract surety volume, rate increases in the

management liability business and lower reinsurance costs primarily resulting from a change in a

reinsurance treaty. Excluding the surety line of business, for which the following are not relevant

measures, business retention rates in 2013 remained strong but were lower than in 2012. Renewal

premium changes in 2013 remained positive and were virtually level with 2012, as increases in renewal

95