Travelers 2001 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2001 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

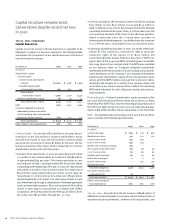

techniques. Our holdings are diversified across industries, and con-

centrations in any one company or industry are limited by

parameters established by senior management as well as by statu-

tory requirements.

Included in our equity portfolio at Dec. 31, 2001 was our investment

in Old Mutual plc, received as partial consideration in our sale of F&G

Life. We are prohibited from selling this for one year from the

Sept. 28, 2001 sale date. To mitigate our exposure to price risk on

this investment, we entered into a collar (embedded in the sale

agreement), as discussed in more detail on page 15 of this report.

During the one-year holding period, changes in the fair value of the

Old Mutual stock will be reflected in unrealized appreciation of

investments, net of tax, in shareholders’ equity. Changes in the fair

value of the collar will be reflected in discontinued operations,

net of tax.

Our portfolio of venture capital investments also has exposure to

market risks, primarily relating to the viability of the various enti-

ties in which we have invested. These investments, primarily in

early-stage companies, involve more risk than other investments

related to downturns in the economy and equity markets, and we

actively manage our market risk in a variety of ways. First, we allo-

cate a comparatively small amount of funds to venture capital. At

the end of 2001, the cost of these investments accounted for only

4% of total invested assets. Second, the investments are diversi-

fied to avoid concentration of risk in a particular industry. Third, we

perform extensive research prior to investing in a new venture to

gauge prospects for success. Fourth, we regularly monitor the oper-

ational results of the entities in which we have invested. Finally, we

generally sell our holdings in these firms soon after they become

publicly traded and when we are legally able to do so, thereby

reducing exposure to further market risk.

At Dec. 31, 2001, our marketable equity securities were recorded at

their fair value of $1.41 billion. A hypothetical 10% decline in each

stock’s price would have resulted in a $141 million impact on

fair value.

At Dec. 31, 2001, our venture capital investments were recorded at

their fair value of $859 million. A hypothetical 10% decline in each

investment’s fair value would have resulted in an $86 million impact

on fair value.

Catastrophe Risk – We manage and monitor our aggregate property

catastrophe exposure through various methods, including pur-

chasing catastrophe reinsurance, establishing underwriting

restrictions and applying a dedicated catastrophe-pricing model.

the st. paul companies

Impact of Accounting Pronouncements to Be Adopted

in the Future

In June 2001, the Financial Accounting Standards Board (FASB)

issued SFAS No. 142, “Goodwill and Other Intangible Assets,” which

establishes financial accounting and reporting for acquired good-

will and other intangible assets. It addresses how intangible assets

that are acquired individually or with a group of other assets (but

not those acquired in a business combination) should be accounted

for in financial statements upon their acquisition. It also addresses

how goodwill and other intangible assets should be accounted for

after they have been initially recognized in the financial statements.

The statement changes current accounting in the way intangible

items with indefinite useful lives, including goodwill, are tested for

impairment on an annual basis. Generally, it also requires that those

assets meeting the criteria for classification as intangible with

estimable useful lives will be amortized, while intangible assets

with indefinite useful lives and goodwill will not be amortized.

Previously, all goodwill was required to be amortized over the esti-

mated useful life, not to exceed 40 years. The statement is effective

for fiscal years beginning after December 15, 2001. We intend to

implement SFAS No. 142 in the period during which its provisions

become effective. We expect our adoption of this statement to result

in a reduction of approximately $30 million in the amount of our

goodwill amortization in 2002, compared with 2001 amortization.

We have not yet determined if we will be required to recognize an

impairment loss on implementation, as a cumulative effect of a

change in accounting principle.

Also in June 2001, the FASB issued SFAS No. 143, “Accounting for

Asset Retirement Obligations,” which establishes financial account-

ing and reporting for obligations associated with the retirement of

tangible long-lived assets and the associated retirement costs. It

requires that the fair value of a liability for an asset retirement obli-

gation be recognized in the period in which it is incurred if a

reasonable estimate of fair value can be made. The associated asset

retirement costs are to be capitalized as part of the carrying amount

of the long-lived asset. This statement is effective for fiscal years

beginning after June 15, 2002. We do not expect the adoption of

SFAS No. 143 to have a material impact on our financial statements.

In August 2001, the FASB issued SFAS No. 144, “Accounting for the

Impairment or Disposal of Long-Lived Assets,” which addresses

financial accounting and reporting for the impairment or disposal

of long-lived assets. This statement supersedes SFAS No. 121,

“Accounting for the Impairment of Long-Lived Assets and for Long-

Lived Assets to be Disposed Of,” and the accounting and reporting

provisions of Accounting Principles Board Opinion No. 30,

“Reporting the Results of Operations – Reporting the Effects of

Disposal of a Segment of a Business, and Extraordinary, Unusual or

Infrequently Occurring Events and Transactions,” for the disposal of

a segment of a business. SFAS No. 144 establishes a single account-

ing model, based on the framework established in SFAS No. 121, for

long-lived assets to be disposed of by sale. It also resolves signifi-

cant implementation issues related to SFAS No. 121. This statement

is effective for fiscal years beginning after December 15, 2001. We

have not yet determined the impact of adopting this statement.

The St. Paul Companies 2001 Annual Report38