Travelers 2001 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2001 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

Life Insurance – Under terms of the F&G Life sale agreement, we

received $335 million in cash and 190,356,631 ordinary shares of

Old Mutual valued at $300 million based on the average closing

price of Old Mutual shares on the London Stock Exchange for the

ten consecutive trading days prior to Sept. 27, 2001. In accordance

with the sale agreement, pretax sales proceeds were reduced by

approximately $12 million, due to a decrease in the market value of

certain securities in F&G Life’s investment portfolio between March

31, 2001 and the closing date of Sept. 28, 2001.

Pursuant to the sale agreement, we must hold the Old Mutual

shares for one year from the closing date. The consideration is sub-

ject to possible adjustment, by means of a collar embedded in the

sale agreement, based on the market value of our Old Mutual

shares at the end of that one-year period. If the market value

exceeds $330 million at that time, we will be required to remit to

Old Mutual either cash or Old Mutual shares in the amount repre-

senting the excess over $330 million. If the market value is less than

$300 million, we will receive cash or Old Mutual shares in the

amount representing the deficit below $300 million, up to a maxi-

mum of $40 million. At Dec. 31, 2001, the market value of the Old

Mutual shares was $242 million. The $58 million decline in market

value was recorded as a component of unrealized appreciation of

investments, net of tax, in shareholders’ equity. The impact of this

unrealized loss was mitigated by the collar, which was estimated to

have a fair value of $17 million at Dec. 31, 2001. That amount was

recorded in our statement of operations in discontinued operations.

We realized a net after-tax loss of $73 million on the sale proceeds.

When the sale agreement with Old Mutual was announced in April

2001, we expected to realize a modest pretax gain on the sale when

proceeds were combined with F&G Life’s operating results through

the disposal date. However, a decline in the market value of certain

F&G Life investments between the April announcement date and

the September closing date, coupled with a change in the antici-

pated tax treatment of the sale, resulted in the net after-tax loss on

the sale proceeds. That loss is combined with F&G Life’s results of

operations prior to sale for an after-tax loss of $54 million and is

included in the reported loss from discontinued operations for the

year ended Dec. 31, 2001.

For the sale of ACLIC, we received cash proceeds of $21 million from

CNA, and we recorded a net after-tax loss on the sale of $1 million.

Nonstandard Auto Insurance – Prudential purchased our nonstan-

dard auto insurance business marketed under the Victoria Financial

and Titan Auto brands for $175 million in cash (net of a $25 million

dividend paid by these operations to our property-liability insur-

ance operations prior to closing). We recorded an estimated

after-tax loss of $83 million on the sale in 1999, representing the

estimated excess of carrying value of these entities at closing date

over proceeds to be received from the sale, plus estimated income

through the disposal date. This excess primarily consisted of good-

will. We recorded an after-tax loss on disposal of $9 million in 2000,

primarily representing additional losses incurred through the dis-

posal date in May, and an additional after-tax loss on disposal of

$5 million in 2001, primarily representing tax adjustments made to

the sale transaction.

Standard Personal Insurance – Metropolitan purchased our stan-

dard personal insurance business operated out of Economy Fire &

Casualty Company and subsidiaries (“Economy”), and the rights

and interests in those non-Economy policies constituting the

remainder of our standard personal insurance operations. Those

rights and interests were transferred to Metropolitan by way of a

reinsurance and facility agreement. We guaranteed the adequacy

of Economy’s loss and loss expense reserves, and we remain liable

for claims on non-Economy policies that result from losses occur-

ring prior to the Sept. 30, 1999 closing date. Under the reserve

guarantee, we will pay for any deficiencies in those reserves and

will share in any redundancies that develop by Sept. 30, 2002. Any

losses incurred by us under these agreements are reflected in dis-

continued operations in the period during which they are incurred.

As of Dec. 31, 2001, our analysis indicated that we will owe

Metropolitan approximately $7 million on these guarantees, and

we recorded a pretax expense equal to that amount in 2001 dis-

continued operations. We also recorded a pretax loss of $14 million

in 2001 related to pre-sale claims. We have no other contingent

liabilities related to this sale.

Minet – In 1997, we sold Minet to Aon Corporation. We recorded a

$9 million pretax expense in discontinued operations in 2001

related to the Minet sale, representing additional funds due Aon

pursuant to provisions of the 1997 sale agreement.

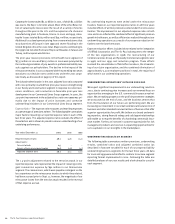

elimination of one-quarter reporting lags

In 2001, we eliminated the one-quarter reporting lag for our primary

underwriting operations in foreign countries (not including our

operations at Lloyd’s), and now report the results of those opera-

tions on a current basis. As a result, our consolidated results for

2001 include their results for the fourth quarter of 2000 and all

quarters of 2001. The incremental impact on our property-liability

operations of eliminating the reporting lag, which consists of the

results of these operations for the three months ended Dec. 31,

2001, was as follows.

Year ended December 31 2001

(In millions)

Net written premiums $71

Net earned premiums 86

GAAP underwriting loss (45)

Net investment income 14

Total pretax loss (31)

The St. Paul Companies 2001 Annual Report 15