Travelers 2001 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2001 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

The St. Paul Companies 2001 Annual Report14

We will continue to maintain appropriate levels of staff to adminis-

ter the settlement of claims incurred in these runoff operations.

• All coverages in our Health Care segment.

• All underwriting operations in Germany, France, the Netherlands,

Argentina, Mexico (excluding surety business, which will con-

tinue), Spain, Australia, New Zealand, Botswana and South Africa.

• In the United Kingdom, all coverages offered to the construction

industry. (Unionamerica, a United Kingdom medical liability

underwriting entity that we acquired in 2000, was placed in

runoff in late 2000, except for business we are contractually

committed to underwrite through Lloyd’s through 2004.)

• At Lloyd’s, casualty insurance and reinsurance, U.S. surplus lines

business, non-marine reinsurance and, when our contractual

commitment expires at the end of 2003, our participation in the

insuring of the Lloyd’s Central Fund.

• In our reinsurance operations, most North American reinsurance

business underwritten in the United Kingdom, all but traditional

finite reinsurance business underwritten by St. Paul Re’s

Financial Solutions business center, bond and credit reinsur-

ance, and aviation reinsurance.

These operations collectively accounted for $1.61 billion, or 22%,

of our net earned premiums, and generated negative underwriting

results totaling $1.5 billion, in 2001 (an amount that does not

include investment income from the assets maintained to support

these operations). They do not qualify as “discontinued operations”

for accounting purposes; therefore, results from these operations

are included in their respective property-liability segment results

discussed on pages 21 to 28 of this report, and will continue to be

reported in those segments during the runoff periods.

In connection with these strategic actions, we wrote off $73 million

of goodwill in the fourth quarter of 2001 related to businesses to be

exited. Approximately $56 million of the write-off related to MMI

Companies, Inc. (“MMI”), $10 million related to operations at Lloyd’s

and the remainder related to our operations in Spain and Australia.

2001 restructuring charge

In December 2001, in connection with our withdrawal from the fore-

going businesses and as part of our overall plan to reduce

company-wide expenses, we announced plans to terminate approx-

imately 1,200 employee positions and reduce the amount of office

space we lease. Of the total positions to be eliminated, approxi-

mately 650 are located in offices outside of the U.S. (most of which

will be closed), approximately 300 are in our Health Care segment

(which has been placed in runoff), and the remaining 250 positions

are spread throughout our domestic operations. In connection with

these actions, we recorded a pretax restructuring charge of

$62 million in the fourth quarter of 2001. The charge included the

following components.

• $46 million of employee-related costs, representing severance

and related benefits to be paid to, or incurred on behalf of, the

estimated total of 800 employees expected to be terminated by

the end of 2002. (Costs associated with the remaining 400

employees were not included in the restructuring charge

because those employees will either be terminated after 2002,

or are employed by one of the operations that may be sold.)

• $9 million of occupancy-related costs, representing excess office

space estimated to be created by the employee terminations.

• $4 million of equipment costs, representing the net carrying

value of computer and other equipment no longer necessary

after terminating employees and vacating office space.

• $3 million of legal costs, representing our estimated fees

payable to outside counsel to obtain regulatory approval to exit

certain states and countries.

No payments were made related to these restructuring actions in

2001. These charges were recorded in our 2001 results as follows:

$42 million in property-liability insurance operations and $20 mil-

lion in “parent company and other operations.”

During 2002, we expect to incur additional employee-related

expenses of approximately $9million related to the 800 employee

positions to be terminated in 2002 when we meet the requirements

to accrue these expenses.

discontinued operations

In September 2001, we completed the sale of Fidelity and Guaranty

Life Insurance Company (“F&G Life”) to Old Mutual plc (“Old

Mutual”), a London-based international financial services company.

Also in September, we sold American Continental Life Insurance

Company (“ACLIC”), a small life insurance company we had

acquired in 2000 as part of our purchase of MMI, to CNA Financial

Corporation (“CNA”). In May 2000, we completed the sale of our

nonstandard auto insurance operations to Prudential Insurance

Company of America (“Prudential”). In 1999, we sold our standard

personal insurance operations to Metropolitan Property and

Casualty Insurance Company (“Metropolitan”). Prior to 1999, we

sold our insurance brokerage operation, Minet Holdings plc

(“Minet”). The results of the operations sold are reflected as dis-

continued operations for all periods presented in this report.

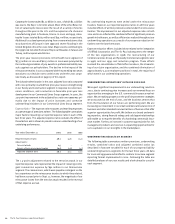

The following table presents the components of discontinued oper-

ations reported in our consolidated statement of operations for

each of the last three years.

Year ended December 31 2001 2000 1999

(In millions)

life insurance:

Operating income, net of taxes $19$43$44

Loss on disposal, net of taxes (74) ––

Total life insurance (55) 43 44

nonstandard auto insurance:

Operating income, net of taxes – – 13

Loss on disposal, net of taxes (5) (9) (83)

Total nonstandard auto insurance (5) (9) (70)

standard personal insurance:

Operating loss, net of taxes – – (22)

Gain (loss) on disposal, net of taxes (13) (11) 177

Total standard personal insurance (13) (11) 155

minet:

Loss on disposal, net of taxes (6) ––

Total Minet (6) ––

Total Discontinued Operations $(79)$23$129