Travelers 2001 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2001 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

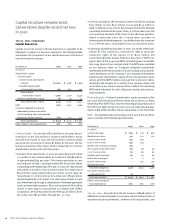

Capital structure remains solid,

conservative despite record net loss

in 2001

the st. paul companies

Capital Resources

Capital resources consist of funds deployed or available to be

deployed to support our business operations. The following table

summarizes the components of our capital resources at the end of

each of the last three years.

December 31 2001 2000 1999

(In millions)

Shareholders’ equity:

Common equity:

Common stock and retained

earnings $4,692 $ 6,481 $ 5,906

Unrealized appreciation

of investments and other 364 697 542

Total common

shareholders’ equity 5,056 7,178 6,448

Preferred shareholders’ equity 58 49 24

Total shareholders’ equity 5,114 7,227 6,472

Debt 2,130 1,647 1,466

Company-obligated mandatorily

redeemable preferred securities

of trusts holding solely subordinated

debentures of the company 893 337 425

Total capitalization $8,137 $ 9,211 $ 8,363

Ratio of debt to total capitalization 26% 18% 18%

Common Equity – Our net loss of $1.09 billion in 2001 was the pri-

mary factor in the 30% decline in common shareholders’ equity

since the end of 2000. In 2000, the 11% increase in common equity

was driven by net income of nearly $1 billion for the year. The fol-

lowing summarizes other major factors impacting our common

shareholders’ equity in the last three years.

• Common share repurchases. In 2001, we repurchased and retired

13.0 million of our common shares for a total cost of $589 million,

or approximately $45 per share. The share repurchases in 2001

occurred prior to Sept. 11 and represented 6% of our total shares

outstanding at the beginning of the year. In 2000, we repurchased

and retired 17.9 million of our common shares for a total cost of

$536 million (approximately $30 per share), and in 1999, we

repurchased 11.1 million shares for a total cost of $356 million

(approximately $32 per share). The share repurchases in each

year were financed through a combination of internally-generated

funds and new debt issuances. Since our issuance of 66.5 million

shares in April 1998 to consummate our merger with USF&G

Corporation, we had repurchased and retired 45.8 million shares

for a total cost of $1.62 billion through Dec. 31, 2001.

• Common dividends. We declared common dividends totaling

$235 million in 2001, $232 million in 2000 and $235 million in

1999. In February 2002, The St. Paul’s board of directors declared

a quarterly dividend of $0.29 per share, a 3.6% increase over the

2001 quarterly dividend of $0.28 per share. We have paid divi-

dends in every year since 1872. During those 130 years of

uninterrupted dividend payments, our dividend rate has increased

in 70 of those years, including the last 16 consecutive years.

• Conversion of preferred securities. In 2000, our wholly-owned sub-

sidiary, St. Paul Capital LLC, exercised its right to cause the

conversion rights of the owners of its $207 million, 6%

Convertible Monthly Income Preferred Securities (“MIPS”) to

expire. Each of the 4,140,000 MIPS outstanding was convertible

into 1.695 shares of our common stock. The MIPS were classified

on our balance sheet as “Company-obligated mandatorily

redeemable preferred securities of trusts holding solely subordi-

nated debentures of the Company,” as a separate line between

liabilities and shareholders’ equity. Prior to the expiration date,

almost all of the MIPS holders exercised their conversion rights,

resulting in the issuance of 7.0 million of our common shares, and

an increase to our common equity of $207 million. The remaining

MIPS were redeemed for cash at $50 per security, plus accumu-

lated dividends.

Preferred Equity – Preferred shareholders’ equity consisted of the

par value of the Series B preferred shares we issued to our Stock

Ownership Plan (SOP) Trust, less the remaining principal balance of

the SOP Trust debt. During 2001 and 2000, we made principal pay-

ments of $14 million and $37 million, respectively, on the Trust debt.

Debt – Consolidated debt outstanding at the end of the last three

years consisted of the following components.

December 31 2001 2000 1999

(In millions)

Commercial paper $ 606 $ 138 $ 400

Medium-term notes 571 617 617

7.875% senior notes 249 249 –

8.125% senior notes 249 249 –

Nuveen line of credit borrowings 183 ––

Zero coupon convertible notes 103 98 94

7.125% senior notes 80 80 80

Variable rate borrowings 64 64 64

Real estate mortgages 2215

8.375% senior notes –150 150

Floating rate notes ––46

Total debt obligations 2,107 1,647 1,466

Fair value of interest rate

swap agreements 23 ––

Total reported debt $2,130 $ 1,647 $ 1,466

Debt as a percentage of

total capitalization 26% 18% 18%

2001 vs. 2000 – Proceeds from the net issuance of $468 million of

additional commercial paper in 2001 were used to fund a portion of

operational cash requirements, common stock repurchases, and

The St. Paul Companies 2001 Annual Report34