Travelers 2001 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2001 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

Catastrophe Risk underwrites commercial property

coverages for major U.S. corporations and personal prop-

erty coverages in certain states exposed to earthquakes

and hurricanes. Ocean Marine provides insurance cover-

age internationally for ocean and inland waterways

traffic. Umbrella/Excess & Surplus Lines underwrites lia-

bility insurance, umbrella and excess liability coverages,

and coverages for unique risks. Oil&Gasprovides spe-

cialized property and casualty products for customers

involved in the exploration and production of oil and gas.

Transportation offers a broad range of coverage options

for the trucking industry. National Programs underwrites

comprehensive insurance programs that are national in

scope. The International Specialty business center is

comprised of specialty insurance business in several for-

eign countries that is managed on a regional basis.

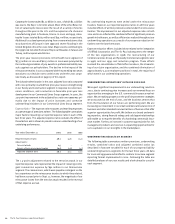

The following table summarizes results for this segment for the last

three years. Data for all three years exclude the impact of the cor-

porate reinsurance program, and data for 2001 also exclude losses

from the terrorist attack. Data including these factors is presented

on page 21 of this report.

Year ended December 31 2001 2000 1999

(Dollars in millions)

Written premiums $2,131 $1,715 $1,361

Percentage increase over prior year 24% 26%

GAAP underwriting result $(81)$ (117) $ (223)

Loss and loss adjustment expense ratio 78.1 78.6 83.4

Underwriting expense ratio 25.3 27.1 32.3

Combined ratio 103.4 105.7 115.7

2001 vs. 2000 – The following discussion analyzes the results of

the respective business centers comprising the Specialty

Commercial segment.

•Financial & Professional Services – Premium volume of $446 mil-

lion in 2001 was 14% higher than 2000 written premiums of

$390 million. The increase was driven by price increases that

averaged 13% for the year, new business in both domestic and

international markets and an incremental $12 million impact

related to our elimination of the one-quarter reporting lag. The

GAAP underwriting loss of $18 million in 2001 improved over the

comparable 2000 loss of $34 million, primarily due to a reduc-

tion in prior-year loss reserves that was partially offset by an

incremental $5 million loss related to our elimination of the one-

quarter reporting lag.

•Technology – Written premiums of $427 million in 2001 grew

24% over comparable 2000 volume of $346 million. The

increase was primarily the result of new business, price

increases averaging 13% for the year and strong renewal reten-

tion rates. The 2001 GAAP underwriting profit of $37 million was

nearly twice the comparable 2000 profit of $19 million, due to

an improvement in current-year loss experience.

•International Specialty – In 2001, written premiums of $319 mil-

lion grew 40% over 2000 premiums of $228 million. The

elimination of the one-quarter reporting lag for a portion of this

business center contributed $38 million of incremental written

premiums in 2001. The remaining growth was centered in

Europe and Canada and was primarily due to price increases.

The GAAP underwriting loss of $97 million in 2001 included $23

million of additional losses resulting from the quarter-lag report-

ing change. Underwriting losses were $94 million in 2000. At the

end of 2001, we announced our intention to withdraw from the

majority of foreign operations that comprise this business center

based on our conclusion that we were unlikely to achieve com-

petitive scale in those geographic locations. We intend to

continue underwriting business in the United Kingdom, Canada

and Ireland.

•Public Sector Services – Written premiums totaled $227 million

in 2001, 29% higher than 2000 premiums of $176 million. In

early 2001, we acquired the right to seek to renew a book of

municipality insurance business from Willis North America Inc.,

which was the primary contributor to premium growth in 2001.

In addition, price increases averaged 11% in this business center

in 2001. The GAAP underwriting profit of $10 million in 2001 was

much improved over the comparable 2000 loss of $10 million,

primarily due to favorable prior-year loss development.

•Umbrella/ Excess & Surplus Lines – Written premiums of

$144 million in 2001 grew 47% over comparable 2000 premium

volume of $98 million. The launch of a new umbrella facility for

retail agents and brokers was the primary contributor to pre-

mium growth in 2001. The GAAP underwriting loss of $36 million

was worse than the 2000 loss of $25 million, primarily due to

adverse prior-year loss development.

•Discover Re – Gross written premiums increased 64% to

$712 million in 2001, and net written premiums of $127 million

grew 33% over 2000 net premium volume of $96 million. Price

increases averaged approximately 25% in 2001, while client

retention ratios exceeded 80%. The GAAP underwriting profit of

$9 million in 2001 was slightly improved over the comparable

2000 profit of $8 million.

•National Programs – Premium volume of $106 million in 2001

was 15% higher than 2000 written premiums of $92 million.

Price increases averaged 19% in 2001, accounting for the major-

ity of premium growth for the year. The 2001 GAAP underwriting

loss of $25 million deteriorated slightly from the comparable

2000 loss of $22 million, primarily due to adverse prior-year loss

development on selected accounts. Current-year loss experience

improved significantly over comparable 2000 results.

The St. Paul Companies 2001 Annual Report22