Pitney Bowes 2010 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2010 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

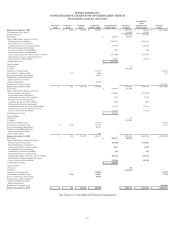

PITNEY BOWES INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Tabular dollars in thousands, except per share data)

44

approach. In the first step, the fair value of each reporting unit is determined. If the fair value of a reporting unit is less than its

carrying value, the second step of the goodwill impairment test is performed to measure the amount of impairment, if any. In the

second step, the fair value of the reporting unit is allocated to the assets and liabilities of the reporting unit as if it had just been

acquired in a business combination, and as if the purchase price was equivalent to the fair value of the reporting unit. The excess of the

fair value of the reporting unit over the amounts assigned to its assets and liabilities is referred to as the implied fair value of goodwill.

The implied fair value of the reporting unit’s goodwill is then compared to the actual carrying value of goodwill. If the implied fair

value is less than the carrying value, an impairment loss is recognized for that excess. The fair values of our reporting units are

determined based on a combination of various techniques, including the present value of future cash flows, multiples of competitors

and multiples from sales of like businesses.

Intangible assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not

be fully recoverable. If such a change in circumstances occurs, the related estimated future undiscounted cash flows expected to result

from the use of the asset and its eventual disposition is compared to the carrying amount. If the sum of the expected cash flows is less

than the carrying amount, an impairment charge is recorded. The impairment charge is measured as the amount by which the carrying

amount exceeds the fair value of the asset. The fair value of the impaired asset is determined using probability weighted expected

cash flow estimates, quoted market prices when available and appraisals as appropriate.

Retirement Plans

Actual pension plan results that differ from our assumptions and estimates are accumulated and amortized over the estimated future

working life of the plan participants and will therefore affect future pension expense. Net pension expense includes current service

costs, interest costs and returns on plan assets. We also base net pension expense primarily on a market related valuation of plan

assets. Under this approach, differences between the actual and expected return on plan assets are recognized over a five-year period.

We recognize the overfunded or underfunded status of pension and other postretirement benefit plans on the Consolidated Balance

Sheets. Gains and losses, prior service costs and credits, and any remaining transition amounts that have not yet been recognized in

net periodic benefit costs are recognized in accumulated other comprehensive income, net of tax, until they are amortized as a

component of net periodic benefit cost. We use a measurement date of December 31 for all of our retirement plans. See Note 19 for

further details.

During 2009, the Board of Directors approved and adopted a resolution amending both U.S. pension plans, the Pitney Bowes Pension

Plan and the Pitney Bowes Pension Restoration Plan, to provide that benefit accruals as of December 31, 2014, will be determined and

frozen and no future benefit accruals under the plans will occur after that date.

Stock-based Compensation

We measure compensation cost for stock-based awards exchanged for employee service at grant date, based on the estimated fair

value of the award, and recognize the cost as expense on a straight-line basis (net of estimated forfeitures) over the employee requisite

service period. We estimate the fair value of stock options using a Black-Scholes valuation model. See Note 12 for further details.

We record deferred tax assets for awards that will result in deductions on our income tax returns, based on the amount of

compensation cost recognized and our statutory tax rate in the jurisdiction in which we will receive a deduction. Differences between

the deferred tax assets recognized for financial reporting purposes and the actual tax deduction reported in our income tax return are

recorded in expense or in capital in excess of par value if the tax deduction exceeds the deferred tax asset or to the extent that

previously recognized credits to paid-in-capital are still available if the tax deduction is less than the deferred tax asset.

Revenue Recognition

We derive our revenue from the sale of equipment, supplies, and software, rentals, financing, and support and business services.

Certain of our transactions are consummated at the same time. The most common form of these transactions involves the sale or lease

of equipment, a meter rental and/or an equipment maintenance agreement. In these cases, revenue is recognized for each of the

elements based on their relative fair values in accordance with the revenue recognition accounting guidance. Fair values of any meter

rental or equipment maintenance agreement are determined by reference to the prices charged in standalone and renewal transactions.

Fair value of equipment is determined based upon the present value of the minimum lease payments. More specifically, revenue

related to our offerings is recognized as follows: