MoneyGram 2015 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2015 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

Table of Contents

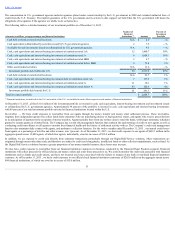

With respect to our credit union customers, our credit exposure is partially mitigated by National Credit Union Administration insurance and we have required

certain credit union customers to provide us with larger balances on deposit and/or to issue cashier’s checks only. While the value of these assets are not at risk in a

disruption or collapse of a counterparty financial institution, the delay in accessing our assets could adversely affect our liquidity and potentially our earnings

depending upon the severity of the delay and corrective actions we may need to take.

While the extent of credit risk may vary by product, the process for mitigating risk is similar. We assess the creditworthiness of each potential agent before

accepting them into our distribution network. This underwriting process includes not only a determination of whether to accept a new agent, but also the remittance

schedule and volume of transactions that the agent will be allowed to perform in a given timeframe. We actively monitor the credit risk of our existing agents by

conducting periodic financial reviews and cash flow analyses of our agents that average high volumes of transactions and monitoring remittance patterns versus

reported sales on a daily basis.

The timely remittance of funds by our agents and financial institution customers is an important component of our liquidity. If the timing of the remittance of funds

were to deteriorate, it would alter our pattern of cash flows and could require us to liquidate investments or utilize our Revolving Credit Facility to settle payment

service obligations. To manage this risk, we closely monitor the remittance patterns of our agents and financial institution customers and act quickly if we detect

deterioration or alteration in remittance timing or patterns. If deemed appropriate, we have the ability to immediately deactivate an agent’s equipment at any time,

thereby preventing the initiation or issuance of further money transfers and money orders.

Credit risk management is complemented through functionality within our point-of-sale system, which can enforce credit limits on a real-time basis. The system

also permits us to remotely disable an agent’s terminals and cause a cessation of transactions.

DerivativeFinancialInstruments — Credit risk related to our derivative financial instruments relates to the risk that we are unable to collect amounts owed to us

by the counterparties to our derivative agreements. Our derivative financial instruments are used to manage exposures to fluctuations in foreign currency exchange

rates. If the counterparties to any of our derivative financial instruments were to default on payments, it could result in a delay or interruption of payments to our

agents. We manage credit risk related to derivative financial instruments by entering into agreements with only major banks and regularly monitoring the credit

ratings of these banks. See Note 6 — DerivativeFinancialInstrumentsof the Notes to the Consolidated Financial Statements for additional disclosure.

Interest Rate Risk

Interest rate risk represents the risk that our operating results are negatively impacted, and our investment portfolio declines in value, due to changes in interest

rates. Given the short maturity profile of the investment portfolio and the low level of interest rates, we believe there is an extremely low risk that the value of these

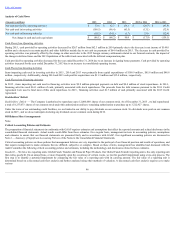

securities would decline such that we would have a material adverse change in our operating results. As of December 31, 2015 , the Company held $372.3 million ,

or 13 percent , of the investment portfolio in fixed rate investments.

At December 31, 2015 , the Company’s other asset-backed securities are priced on average at $0.04 per dollar of par value for a total fair value of $11.6 million .

Included in other asset-backed securities are collateralized debt obligations backed primarily by high-grade debt, mezzanine equity tranches of collateralized debt

obligations and home equity loans, along with private equity investments. Any resulting adverse movement in our stockholders’ deficit or settlement assets from

declines in investments would not result in regulatory or contractual compliance exceptions.

Our operating results are impacted by interest rate risk through our net investment margin, which is investment revenue less investment commissions expense. As

the money transfer business is not materially affected by investment revenue and pays commissions that are not tied to an interest rate index, interest rate risk has

the most impact on our money order and official check businesses. We are invested primarily in interest-bearing deposit accounts, non-interest bearing transaction

accounts, U.S. government money market securities, time deposits and certificates of deposit. These types of investments have minimal risk of declines in fair

value from changes in interest rates. Our commissions paid to financial institution customers are variable rate, based primarily on the federal funds effective rate

and are reset daily. Accordingly, both our investment revenue and our investment commissions expense will decrease when rates decline and increase when rates

rise. In the current environment, the federal funds effective rate is so low that many of our financial institution customers are in a “negative” commission position,

and therefore, we do not owe any commissions to these customers.

Our results are impacted by interest rate risk through our interest expense for borrowings under the 2013 Credit Agreement. The Company may elect an interest

rate for its debt under the 2013 Credit Agreement at each reset period based on the BOA prime bank rate or the Eurodollar rate. The interest rate election may be

made individually for the Term Credit Facility and each draw under the Revolving Credit Facility. The interest rate will be either the “alternate base rate”

(calculated in part based on the BOA prime rate) plus either 200 or 225 basis points (depending on the Company's secured leverage ratio or total leverage ratio, as

applicable, at such time) or the Eurodollar rate plus either 300 or 325 basis points (depending on the Company's secured leverage ratio or total leverage ratio, as

applicable, at such time). In connection with the initial funding under the 2013 Credit Agreement,

52