IHOP 2010 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2010 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

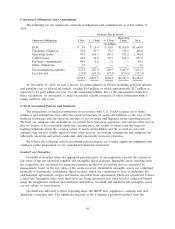

November 29, 2007 acquisition of Applebee’s and has been allocated between the two Applebee’s units.

The Company tests goodwill and other indefinite life intangible assets for impairment on an annual

basis in the fourth quarter. The annual impairment test of goodwill of the two Applebee’s units is

performed as of October 31 of each year. The annual impairment test of the goodwill of the IHOP unit

is performed as of December 31 of each year, the date as of which the analysis has been performed in

prior years. In addition to the annual test of impairment, goodwill and indefinite life intangible assets

must be evaluated more frequently if the Company believes indicators of impairment exist. Such

indicators include, but are not limited to, events or circumstances such as a significant adverse change

in the business climate, unanticipated competition, a loss of key personnel, adverse legal or regulatory

developments, or a significant decline in the market price of the Company’s common stock.

In the process of the Company’s annual impairment review of goodwill, the Company primarily

uses the income approach method of valuation that includes the discounted cash flow method as well

as other generally accepted valuation methodologies to determine the fair value. Significant

assumptions used to determine fair value under the discounted cash flows model include future trends

in sales, operating expenses, overhead expenses, depreciation, capital expenditures, and changes in

working capital along with an appropriate discount rate. Additional assumptions are made as to

proceeds to be received from future franchising of company-operated restaurants. Step one of the

impairment test compares the fair value of each of our reporting units to its carrying value. If the fair

value is in excess of the carrying value, no impairment exists. If the step one test does indicate an

impairment, step two must take place. Under step two, the fair value of the assets and liabilities of the

reporting unit are estimated as if the reporting unit were acquired in a business combination. The

excess of the fair value of the reporting unit over the carrying amounts assigned to its assets and

liabilities is the implied fair value of the goodwill, to which the carrying value of the goodwill must be

adjusted. The fair value of all reporting units is then compared to the current market value of the

Company’s common stock to determine if the fair values estimated in the impairment testing process

are reasonable in light of the current market value.

In the process of the Company’s annual impairment review of the tradename, the most significant

indefinite life intangible asset, the Company primarily uses the relief of royalty method under income

approach method of valuation. Significant assumptions used to determine fair value under the relief of

royalty method include future trends in sales, a royalty rate and a discount rate to be applied to the

forecast revenue stream.

Long-Lived Assets

We assess long-lived and intangible assets with finite lives for impairment when events or changes

in circumstances indicate that the carrying value of the assets may not be recoverable. We test

impairment using historical cash flows and other relevant facts and circumstances as the primary basis

for our estimates of future cash flows. We consider factors such as the number of years the restaurant

has been operated by us, sales trends, cash flow trends, remaining lease life, and other factors which

apply on a case-by-case basis. The analysis is performed at the individual restaurant level for indicators

of permanent impairment. Recoverability of the restaurant’s assets is measured by comparing the assets’

carrying value to the undiscounted cash flows expected to be generated over the assets’ remaining

useful life or remaining lease term, whichever is less. If the total expected undiscounted future cash

flows are less than the carrying amount of the assets, the carrying amount is written down to the

estimated fair value, and a loss resulting from impairment is recognized by charging to earnings. This

process requires the use of estimates and assumptions, which are subject to a high degree of judgment.

If these assumptions change in the future, we may be required to record impairment charges for these

assets.

69