IHOP 2010 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2010 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

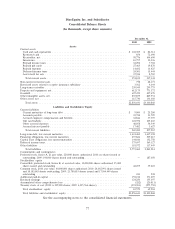

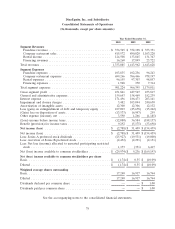

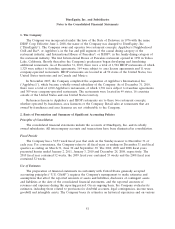

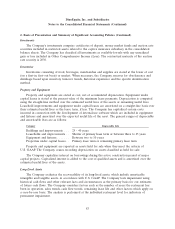

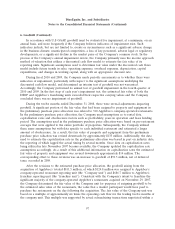

DineEquity, Inc. and Subsidiaries

Notes to the Consolidated Financial Statements (Continued)

2. Basis of Presentation and Summary of Significant Accounting Policies (Continued)

The rental payments or receipts on those property leases that meet the capital lease criteria will

result in the recognition of interest expense or interest income and a reduction of capital lease

obligation or financing lease receivable. Capital lease obligations are amortized based on the

Company’s incremental borrowing rate and direct financing leases are amortized using the implicit

interest rate.

The lease term used for straight-line rent expense is calculated from the date the Company obtains

possession of the leased premises through the lease termination date. The Company expenses rent from

possession date through restaurant open date as expense. Once a restaurant opens for business, the

Company records straight-line rent over the lease term plus contingent rent to the extent it exceeded

the minimum rent obligation per the lease agreement. The Company uses a consistent lease term when

calculating depreciation of leasehold improvements, when determining straight-line rent expense and

when determining classification of its leases as either operating or capital. For leases that contain rent

escalations, the Company records the total rent payable during the lease term, as determined above, on

the straight-line basis over the term of the lease (including the rent holiday period beginning upon our

possession of the premises), and records the difference between the minimum rents paid and the

straight-line rent as a lease obligation. Certain leases contain provisions that require additional rental

payments based upon restaurant sales volume (‘‘contingent rent’’). Contingent rentals are accrued each

period as the liabilities are incurred, in addition to the straight-line rent expense noted above.

Certain lease agreements contain tenant improvement allowances, rent holidays and lease

premium, which are amortized over the shorter of the estimated useful life or lease term. For tenant

improvement allowances, the Company also records a deferred rent liability or an obligation in our

non-current liabilities on the consolidated balance sheets and amortizes the deferred rent over the term

of the lease as a reduction to company restaurant expenses in the consolidated statements of

operations.

Preopening Expenses

Expenditures related to the opening of new or relocated restaurants are charged to expense when

incurred.

Advertising

Franchise fees designated for IHOP’s national advertising fund and local marketing and advertising

cooperatives are recognized as revenue as the fees are earned and become receivables from the

franchisee in accordance with U.S. GAAP governing the accounting for franchise fee revenue. In

accordance with U.S. GAAP governing advertising costs, related advertising obligations are accrued and

the costs expensed at the same time the related revenue is recognized. Franchise fees designated for

Applebee’s national advertising fund and local advertising cooperatives constitute agency transactions

and are not recognized as revenues and expenses. In both cases, the advertising fees are recorded as a

liability against which specific costs are charged.

Advertising expense reflected in the consolidated statements of operations includes local marketing

advertising costs incurred by company-operated restaurants, contributions to the national advertising

fund made by Applebee’s company-operated restaurants and certain advertising costs incurred by the

Company to benefit future franchise operations. Costs of advertising are expensed either as incurred or

the first time the advertising takes place. Advertising expense included in company restaurant

87