IHOP 2010 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2010 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

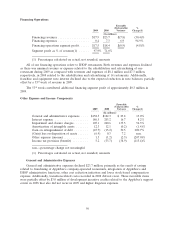

Partially offsetting these increases were the absence of one-time costs of $6.3 million incurred in

February 2009 related to the establishment of a purchasing co-operative and lower professional services

expenses.

Interest Expense

The $15.0 million decrease in interest expense is primarily due to the retirement of long-term debt

prior to the October 2010 Refinancing and lower non-cash amortization of deferred financing costs

subsequent to the October 2010 Refinancing. During 2010 and 2009, we retired $280 million of

Series 2007-1 Class A-2-II-X and Series 2007-1 Class A-2-II-A Senior Notes carrying fixed interest rates

of approximately 7.1%. Based on the average balances of debt outstanding over the respective years,

interest expense was approximately $9 million lower in 2010 because of the retirements.

Non-cash amortization of deferred financing costs, debt discount and effective portion of loss on

an interest swap was approximately $40 million per year prior to the October 2010 Refinancing, while

non-cash amortization of deferred financing costs and debt discount is approximately $6 million per

year after the October 2010 Refinancing.

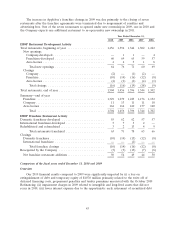

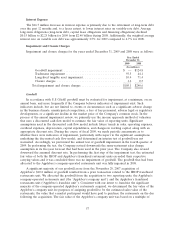

Impairment and Closure Charges

Impairment and closure charges for the years ended December 31, 2010 and 2009 were as follows:

Year Ended

December 31,

2010 2009

(In millions)

Tradename impairment ................................ $— $ 93.5

Long-lived tangible asset impairment ...................... 1.5 10.4

Closure charges ...................................... 2.0 1.2

Total impairment and closure charges ........................ $3.5 $105.1

Goodwill

In accordance with U.S GAAP, goodwill must be evaluated for impairment, at a minimum, on an

annual basis, and more frequently if we believe indicators of impairment exist. Such indicators include,

but are not limited to, events or circumstances such as a significant adverse change in the business

climate, unanticipated competition, a loss of key personnel, adverse legal or regulatory developments,

or a significant decline in the market price of our common stock. In the process of the annual

impairment review, we primarily use the income approach method of valuation that uses a discounted

cash flow model to estimate the fair value of reporting units. Significant assumptions used in the

discounted cash flow model include future trends in sales, operating expenses, overhead expenses,

depreciation, capital expenditures, and changes in working capital, along with an appropriate discount

rate. During the course of fiscal 2010 and 2009 we made periodic assessments as to whether there were

indicators of impairment, particularly with respect to the significant assumptions underlying the

discounted cash flow model. In each year we determined an interim test of goodwill was not warranted.

Accordingly, we performed the annual test of goodwill impairment in the fourth quarter of 2010 and

2009. In performing the first step of the impairment test, the estimated fair value of both the IHOP

and Applebee’s franchised restaurant units exceeded their respective carrying values and we concluded

there was no impairment of goodwill in either 2010 or 2009.

49