IHOP 2010 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2010 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

Liquidity and Capital Resources of the Company

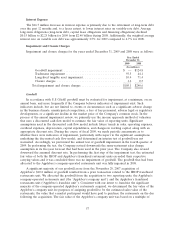

We incurred approximately $2.3 billion of securitized indebtedness in connection with the 2007

acquisition of Applebee’s, of which approximately $1.6 billion remained outstanding as of October 19,

2010. This indebtedness had an accelerated repayment date of 2012, subject to certain short-term

extensions.

Credit Facilities

On October 8, 2010, we entered into a credit agreement with a group of lenders and financial

institutions (the ‘‘Credit Agreement’’) that established a senior secured credit facility (the ‘‘Senior

Secured Credit Facility’’) consisting of a $900 million term facility (the ‘‘Term Facility’’) maturing in

October 2017 and a $50 million senior secured revolving credit facility (the ‘‘Revolving Facility’’)

maturing in October 2015. Loans made under the Term Facility and the Revolving Facility will bear

interest, at our option, at an annual rate equal to (i) a LIBOR based rate (which will be subject to a

floor of 1.50%) plus a margin of 4.50% or (ii) the base rate (the ‘‘Base Rate’’) (which will be subject to

a floor of 2.50%), which will be equal to the highest of (a) the federal funds rate plus 0.50%, (b) the

prime rate and (c) the one month LIBOR rate (which will be subject to a floor of 1.50%) plus 1.00%,

plus a margin of 3.50%. As of December 31, 2010, the interest rate on the Term Facility was 6.0%. The

margin for the Revolving Facility is subject to debt leverage-based step-downs.

The Revolving Facility is utilized, among other purposes, to collateralize certain letters of credit we

are required to maintain that were previously collateralized with restricted cash. Such collateralization

does not constitute a draw-down under the Revolving Facility but does reduce the amount that can be

borrowed under the Revolving Facility. Unused amounts of the Revolving Facility bear interest at the

rate of 75 basis points per annum. As of December 31, 2010, no amounts were borrowed under the

Revolving Facility and approximately $25 million in letters of credit were collateralized by the

Revolving Facility.

The Credit Agreement also provides for an uncommitted incremental facility that permits the

Company, subject to certain conditions, to increase the Senior Secured Credit Facility by up to

$250 million; provided that the aggregate amount of the commitments under the Revolving Facility may

not exceed $150 million.

October 2010 Refinancing

On October 20, 2010, we completed a refinancing of our $1.6 billion of securitized indebtedness

using the following sources of funds:

• We borrowed $900 million under the Term Facility; and

• We issued $825 million of senior unsecured notes (the ‘‘Notes’’) at par that will mature in

October 2018 with a coupon of 9.5% per annum. Interest on the Company’s bonds is payable in

the months of April and October of each year, beginning in April 2011.

These borrowings, along with cash on hand not required for operating needs and previously

restricted cash becoming available concurrently with the retirement of the securitized debt totaled

approximately $1.85 billion.

We used these funds in the following manner:

• Repaid the entire $1.6 billion face value of securitized indebtedness outstanding as of

October 19, 2010;

• Paid $46.1 million of prepayment costs and tender premiums associated with the retirement;

• Redeemed 143,000 shares of our Series A Stock for $143 million;

62