Honeywell 2012 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2012 Honeywell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

|

|

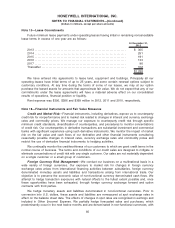

Committee of the Board. The exercise price of stock options is set on the grant date and may not be

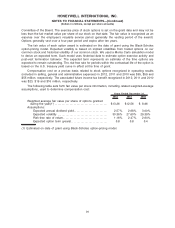

less than the fair market value per share of our stock on that date. The fair value is recognized as an

expense over the employee’s requisite service period (generally the vesting period of the award).

Options generally vest over a four-year period and expire after ten years.

The fair value of each option award is estimated on the date of grant using the Black-Scholes

option-pricing model. Expected volatility is based on implied volatilities from traded options on our

common stock and historical volatility of our common stock. We used a Monte Carlo simulation model

to derive an expected term. Such model uses historical data to estimate option exercise activity and

post-vest termination behavior. The expected term represents an estimate of the time options are

expected to remain outstanding. The risk-free rate for periods within the contractual life of the option is

based on the U.S. treasury yield curve in effect at the time of grant.

Compensation cost on a pre-tax basis related to stock options recognized in operating results

(included in selling, general and administrative expenses) in 2012, 2011 and 2010 was $65, $59 and

$55 million, respectively. The associated future income tax benefit recognized in 2012, 2011 and 2010

was $23, $19 and $16 million, respectively.

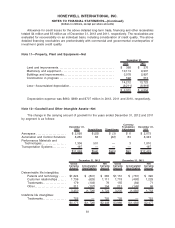

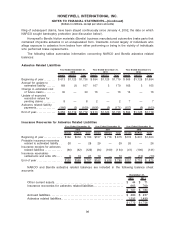

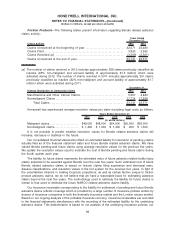

The following table sets forth fair value per share information, including related weighted-average

assumptions, used to determine compensation cost:

2012 2011 2010

Years Ended December 31,

Weighted average fair value per share of options granted

during the year(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $13.26 $12.56 $ 8.96

Assumptions:

Expected annual dividend yield. . . . . . . . . . . . . . . . . . . . . . . . . 2.57% 2.68% 3.00%

Expected volatility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30.36% 27.60% 29.39%

Risk-free rate of return. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.16% 2.47% 2.64%

Expected option term (years). . . . . . . . . . . . . . . . . . . . . . . . . . . 5.8 5.8 5.4

(1) Estimated on date of grant using Black-Scholes option-pricing model.

91

HONEYWELL INTERNATIONAL INC.

NOTES TO FINANCIAL STATEMENTS—(Continued)

(Dollars in millions, except per share amounts)