ICICI Bank 2005 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2005 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

33

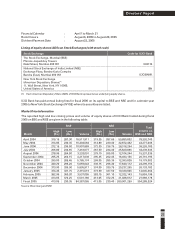

Business Overview

The Retail Banking Group (RBG) is responsible for our products and services for retail customers and small

and medium enterprises including various credit products, liability products (including our own products

as well as distribution of third party liability products) and transaction banking services.

The Wholesale Banking Group (WBG) is responsible for our products and services for corporate clients,

including credit and treasury products, project finance, structured finance and transaction banking

services. This group is also responsible for our securitisation activities. The Rural, Micro-banking & Agri-

business Group (RMAG) forms part of WBG.

The International Business Group (IBG) is responsible for our international operations, including our

operations in various overseas markets as well as our products and services for non-resident Indians

(NRIs) and our international trade finance and correspondent banking relationships.

The Corporate Centre comprises all shared services and corporate functions, including finance and

balance sheet management, secretarial, investor relations, risk management, legal, human resources and

corporate branding and communications. A separate team within the Corporate Centre is responsible for

our proprietary trading activities.

In addition to the above, there are certain specialised groups namely, Technology Management Group

(TMG) which is responsible for enterprise-wide technology initiatives, Organisational Excellence Group

(OEG) which is responsible for quality initiatives and Social Initiatives Group (SIG) which is responsible for

our social and community development activities.

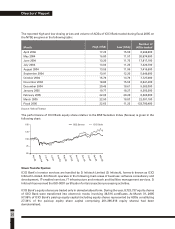

BUSINESS REVIEW

During fiscal 2005, ICICI Bank continued to grow and diversify its asset base and revenue streams by

leveraging the growth platforms created over the past few years. We consolidated our leadership position

in retail credit, achieved robust growth in our fee income from both corporate and retail customers, grew

our deposit base and significantly scaled up our international operations.

Retail Banking

We entered the retail business in 1998 and it has been a key driver of our growth since 2001. While we were

among the first banks to identify the growth potential of retail credit in India, over the last two years the

banking system as a whole has seen significant expansion of retail credit, with retail loans accounting for a

major part of overall systemic credit growth. We believe that the systemic growth is driven by sound

fundamentals, namely, rising income levels, favourable demographic profile and wide availability and

affordability of credit. At the same time, the retail credit business requires a high level of credit and

analytical skills and strong operations processes backed by technology. Our retail strategy is centred

around a wide distribution network, leveraging our branches and offices, direct marketing agents and

manufacturer, dealer and real estate developer relationships; a comprehensive and competitive product

suite; technology-enabled back-office processes and a robust credit and analytical framework.

We are the largest provider of retail credit in India and have the largest retail loan portfolio among banks in

the country. In fiscal 2005, we maintained and enhanced our market leadership in every segment of the

retail credit business, including home loans, car loans, personal loans and credit cards. Our total retail

disbursements in fiscal 2005 were approximately Rs. 433.00 billion, compared to approximately Rs. 288.00

billion in fiscal 2004. Our total retail portfolio increased from Rs. 334.23 billion at March 31, 2004 to

Rs. 561.33 billion at March 31, 2005, constituting 61% of loans. We continued our focus on retail deposits to

create a stable funding base. At March 31, 2005 we had over 13 million retail customer accounts.

Dickenson Tel: 022-2625 2282