ICICI Bank 2005 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2005 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

32

FINANCIAL SECTOR OVERVIEW

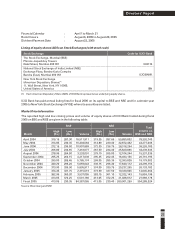

The financial sector witnessed significant developments during fiscal 2005. Credit growth strengthened

with an increase in industrial activity. Non-food credit increased by 29.1% in fiscal 2005 compared to

18.5% in fiscal 2004. Based on data published by RBI, the industrial sector is estimated to have accounted

for 27.0% of credit growth in fiscal 2005 as compared to 16.0% in fiscal 2004. The contribution of retail

credit growth to overall credit growth was the largest at 42.0% of total non-food credit. The credit-deposit

ratio increased from about 56.0% in April 2004 and stood at about 60.0% from November 2004 onwards.

The incremental credit deposit ratio, excluding the impact of conversion of IDBI into a bank, was about

100.0% in March 2005 compared to about 60.0% at the beginning of the year. Deposit grew by Rs. 2,285.26

billion, or 14.5%, in fiscal 2005 compared to 16.2% in fiscal 2004. The average yield on 10-year

government securities increased from 5.5% in fiscal 2004 to 6.2% in fiscal 2005. In response to the hike in

CRR and the reverse repo rate in the RBI’s mid-year review, in November 2004, banks increased their

benchmark prime lending and deposit rates.

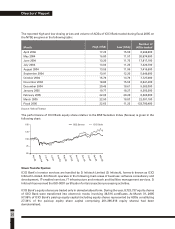

Growth in both the life and non-life insurance markets was significant. First year premium underwritten in

the life insurance sector recorded a growth of 35.7% to reach Rs. 253.43 billion in fiscal 2005 with the

private sector’s market share increasing from 13.0% in fiscal 2004 to 21.9% in fiscal 2005. Gross premium

in the non-life insurance sector grew by 12.8% to Rs. 180.95 billion in fiscal 2005 with the private sector’s

market share increasing from 14.1% in fiscal 2004 to 19.6% in fiscal 2005. Total assets under management

of mutual funds grew by 7.2% from Rs. 1,396.16 billion at March 31, 2004 to Rs. 1,496.00 billion at

March 31, 2005.

The banking sector witnessed several important regulatory developments. In June 2004, guidelines on

capital for market risk were issued. Under this, banks would be required to maintain a capital charge for

market risk in respect of their trading and available for sale investment portfolios. RBI has issued draft

guidelines for the implementation of the revised capital adequacy framework of the Basel Committee.

These are to be effective from fiscal 2007 and prescribe a 75.0% weight for retail credit exposure, rating

based differential risk weights for other credit exposures and a capital charge for operational risk. A

roadmap for the presence of foreign banks in India has also been outlined. Initially, foreign banks are

allowed entry only in private sector banks identified by RBI for restructuring in which acquisition is allowed

in a phased manner. On February 28, 2005, RBI released guidelines on ownership and governance in

private sector banks.

The Indian financial sector is rapidly moving towards international benchmarks. Progress in the direction

of increasing efficiency, transparency and dynamism in the system has been rapid. Given the rapid growth

prospects in India, the financial sector has a crucial role to play in the development of the economy. Broad

based reforms have made the banking sector competitive and have positioned it well to support

sustainable growth in a fast growing economy.

ORGANISATION STRUCTURE

Our organisation structure is designed to be flexible and customer-focused, while seeking to ensure

effective control and supervision and consistency in standards across the organisation and align all areas

of operations to overall organisational objectives. The organisation structure is divided into four principal

groups - Retail Banking, Wholesale Banking, International Business and Corporate Centre.

Business Overview

Dickenson Tel: 022-2625 2282