ICICI Bank 2005 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2005 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

F55

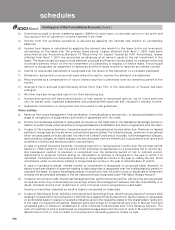

After impairment, depreciation is provided on the revised carrying amount of the assets over its remaining useful

life. A previously recognised impairment loss is increased or reversed depending on changes in circumstances.

However the carrying value after reversal is not increased beyond the carrying value that would have prevailed by

charging usual depreciation if there was no impairment. As on March 31, 2005 there were no events or changes in

circumstances, which indicate any impairment in the carrying value of the assets covered by AS 28.

12. Accounting for contingencies

The Bank estimates the probability of any loss that might be incurred on outcome of contingencies on the basis of

information available up to the date on which the financial statements are prepared. A provision is recognised when

an enterprise has a present obligation as a result of past event and it is probable that an outflow of resources will be

required to settle the obligation, in respect of which a reliable estimate can be made. Provisions are determined

based on management estimate required to settle the obligation at the balance sheet date, supplemented by

experience of similar transactions. These are reviewed at each balance sheet date and adjusted to reflect the

current management estimates. In cases where the available information indicates that the loss on the contingency

is reasonably possible but the amount of loss cannot be reasonably estimated, a disclosure is made in the financial

statements. In case of remote possibility neither provision nor disclosure is made in the financials.

13. Earnings per share

Basic and diluted earnings per share are calculated by dividing the net profit or loss for the period attributable to

equity shareholders by the weighted average number of equity shares outstanding during the period. Diluted

earnings per equity share has been computed using the weighted average number of equity shares and dilutive

potential equity shares outstanding during the period, except where the results are anti-dilutive.

14. Cash and cash equivalents

Cash and cash equivalents include cash in hand, balances with RBI, balances with other banks and money at call and

short notice.

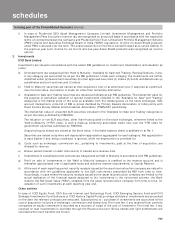

15. Others

a. Reinsurance premium of insurance business

In case of general insurance business, insurance premium on ceding of the risk is recognised in the year in

which the risk commences. Any subsequent revision to premium ceded is recognised in the year of revision.

Adjustment to reinsurance premium arising on cancellation of policies is recognised in the year in which it is

cancelled. In case of life insurance business, reinsurance premium ceded is accounted in accordance with the

treaty or in-principle arrangement with the reinsurer.

b. Claims and benefits paid

In case of general insurance business, claims comprise claims paid, estimated liability for outstanding claims

made following a loss occurrence reported and estimated liability for claims Incurred But Not Reported ('IBNR')

and claims Incurred But Not Enough Reported ('IBNER'). Further, claims incurred also include specific claim

settlement costs such as survey / legal fees and other directly attributable costs.

Claims (net of amounts receivable from reinsurers/coinsurers) are recognised on the date of intimation of the

loss.

Estimated liability for outstanding claims at Balance Sheet date is recorded net of claims recoverable from/

payable to co-insurers/reinsurers and salvage to the extent there is certainty of realisation. Estimated liability

for outstanding claims is determined by management on the basis of ultimate amounts likely to be paid on each

claim based on past experience. These estimates are progressively revalidated on availability of further

information.

IBNR represents that amount of claims that may have been incurred during the accounting period but have not

been reported or claimed. The IBNR provision also includes provision, if any, required for claims IBNER.

IBNR/IBNER liabilities are based on an actuarial estimate duly certified by the Appointed Actuary of the company.

In case of life insurance business, claims other than maturity claims are accounted for on receipt of intimation.

Maturity claims are accounted when due for payment. Reinsurance on such claims is accounted for, in the same

period as the related claims. Withdrawals under linked policies are accounted in the respective schemes.

c. Reserve for unexpired risk

Reserve for unexpired risk is recognised net of reinsurance ceded and represents premium written that is

attributable and to be allocated to succeeding accounting periods for risks to be borne by the company

schedules

forming part of the Consolidated Accounts (Contd.)