Volvo 2010 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2010 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

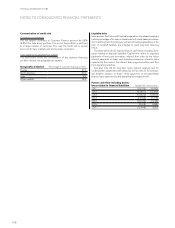

NOTE 35 FEES TO THE AUDITORS

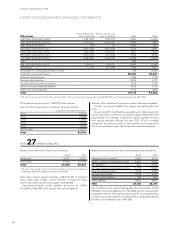

Fees to the auditors 2009 2010

PricewaterhouseCoopers

- Audit fees 110 102

- Audit-related fees 7 6

- Tax advisory services 14 16

- Other fees 3 3

Total 134 127

Audit fees to others 1 1

Volvo Group Total 135 128

Audit involves examination of the annual report and financial account-

ing and the administration by the Board and the President. Audit-

related assignments mean quality assurance services required by

enactment, articles of association, regulations or agreement. The

amount includes among other things the fee for the half-year review.

Tax services include both tax consultancy and tax compliance ser-

vices. All other tasks are defined as other. 2009 figures are restated

for comparability.

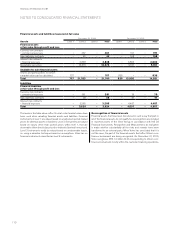

NOTE 36 GOALS AND POLICIES IN FINANCIAL RISK MANAGEMENT

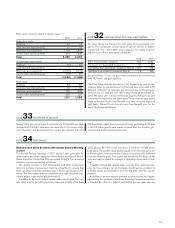

Apart from derivatives, Volvo’s financial instruments consist of bank

loans, finance leasing contracts, accounts payable, accounts receiva-

ble, shares and participations, as well as cash and short-term invest-

ments.

The primary risks deriving from the handling of financial instru-

ments are interest-rate risk, currency risk, liquidity risk and credit risk.

All of these risks are handled in accordance with an established finan-

cial policy.

Interest-rate risks

Interest-rate risk refers to the risk that changed interest-rate levels will

affect consolidated earnings and cash flow (cash-flow risks) or the fair

value of financial assets and liabilities (price risks). Matching the inter-

est-fixing terms of financial assets and liabilities reduces the ex posure.

Interest-rate swaps are used to change/influence the interest-fixing

term for the Group’s financial assets and liabilities. Currency interest-

rate swaps permit borrowing in foreign currencies from different mar-

kets without introducing currency risk. Volvo also has standardized

interest-rate forward contracts (futures) and FRAs (forward-rate

agreements). Most of these contracts are used to hedge interest-rate

levels for short-term borrowing or investment.

Cash-flow risks

The effect of changed interest-rate levels on future currency and

interest-rate flows refers mainly to the Group’s customer financing

operations and net financial items. Within the customer finance oper-

ations the degree of matching interest-rate fixing on borrowing and

lending is measured. The calculation of the matching degree excludes

equity, which in the customer finance operations amount to between

8 and 10%. According to the Group’s policy, the degree of matching

for interest-rate fixing on borrowing and lending in the customer-

financing operations must exceed 80%. At year-end 2010, the degree

of such matching was 100% (100). A part of the short-term financing

of the customer financing operations can however be pertaining to

internal loans from the industrial operations, why the matching ratio in

the Volvo group then may be slightly lower. At year-end 2010, in addi-

tion to the assets in its customer-financing operations, Volvo’s inter-

est-bearing assets consisted primarily of cash, cash equivalents and

liquid assets invested in short-term interest-bearing securities. The

objective is to achieve an interest-fixing term of three months for the

liquid assets in Volvo’s industrial operations through the use of deriva-

tives. On December 31, 2010, after taking derivatives into account,

the average interest on these assets was 2.0% (1.1). After taking

derivatives into account, outstanding loans had interest terms corre-

sponding to an interest-rate fixing term of three months and the aver-

age interest at year-end amounted to 4.3% (4.1).

Price risks

Exposure to price risks as result of changed interest-rate levels refers

to financial assets and liabilities with a longer interest-rate fixing term

(fixed interest). A comparison of the reported values and the fair val-

ues of all of Volvo’s financial assets and liabilities, as well as its deriva-

tives, is provided in note 37, Financial instruments.

Assuming that the market interest rates for all currencies suddenly

rose by one percentage point (100 interest-rate points) over the inter-

est-rate level on December 31, 2010, for the next 12-month period, all

other variables remaining unchanged, Volvo’s net interest income

would be negatively impacted by 295 (neg: 354) considering an inter-

est rate fixing term of three months for receivables and liabilities.

Assuming that the market interest rates for all currencies fell in a

similar manner by one percentage point (100 interest-rate points),

Volvo’s net interest income would be positively impacted by a corre-

sponding amount.

The following table shows the effect on income before taxes in

Volvo’s key financing currencies if the interest-rate level were to

increase by one percentage point, (100 interest-rate points) not con-

sidering interest rate fixing terms.

SEK M Effect on income

SEK (46)

USD (76)

EUR 55

CNY 17

JPY (221)

INR 13

The above sensitivity analysis is based on assumptions that rarely

occur in reality. It is not unreasonable that market interest rates

change with one percentage point (100 interest-rate points) over a

12-month period. However, in reality, market interest rates usually do

not rise or fall at one point in time. Moreover, the sensitivity analysis

also assumes a parallel shift in the yield curve and an identical effect

105