US Airways 2009 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2009 US Airways annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

Table of Contents

whether a reporting entity is required to consolidate another entity is based on, among other things, the other entity's purpose and design

and the reporting entity's ability to direct the activities of the other entity that most significantly impact the other entity's economic

performance. ASU No. 2009-17 will require a reporting entity to provide additional disclosures about its involvement with variable

interest entities and any significant changes in risk exposure due to that involvement. A reporting entity will be required to disclose how

its involvement with a variable interest entity affects the reporting entity's financial statements. ASU No. 2009-17 is effective for fiscal

years beginning after November 15, 2009, and interim periods within those fiscal years. The Company is currently evaluating the

requirements of ASU No. 2009-17 and has not yet determined the impact on its consolidated financial statements.

In October 2009, the FASB issued ASU No. 2009-13, "Revenue Recognition (Topic 605) – Multiple-Deliverable Revenue

Arrangements." ASU No. 2009-13 addresses the accounting for multiple-deliverable arrangements to enable vendors to account for

products or services (deliverables) separately rather than as a combined unit. This guidance establishes a selling price hierarchy for

determining the selling price of a deliverable, which is based on: (a) vendor-specific objective evidence; (b) third-party evidence; or

(c) estimates. This guidance also eliminates the residual method of allocation and requires that arrangement consideration be allocated at

the inception of the arrangement to all deliverables using the relative selling price method. In addition, this guidance significantly

expands required disclosures related to a vendor's multiple-deliverable revenue arrangements. ASU No. 2009-13 is effective

prospectively for revenue arrangements entered into or materially modified in fiscal years beginning on or after June 15, 2010 and early

adoption is permitted. A company may elect, but will not be required, to adopt the amendments in ASU No. 2009-13 retrospectively for

all prior periods. The Company is currently evaluating the requirements of ASU No. 2009-13 and has not yet determined the impact on

the Company's consolidated financial statements.

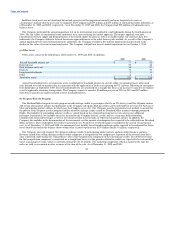

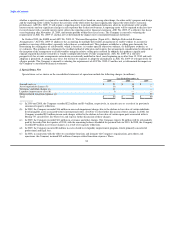

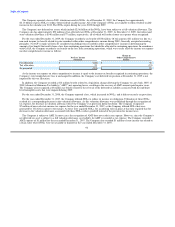

2. Special Items, Net

Special items, net as shown on the consolidated statements of operations include the following charges (in millions):

Year Ended December 31,

2009 2008 2007

Aircraft costs (a) $ 22 $ 14 $ —

Asset impairment charges (b) 16 18 —

Severance and other charges (c) 11 9 —

Liquidity improvement costs (d) 6 — —

Merger-related transition expenses (e) — 35 99

Total $ 55 $ 76 $ 99

(a) In 2009 and 2008, the Company recorded $22 million and $14 million, respectively, in aircraft costs as a result of its previously

announced capacity reductions.

(b) In 2009, the Company recorded $16 million in non-cash impairment charges due to the decline in fair value of certain indefinite

lived intangible assets associated with its international routes. See Note 1(i) for further discussion of these charges. In 2008, the

Company recorded $18 million in non-cash charges related to the decline in fair value of certain spare parts associated with its

Boeing 737 aircraft fleet. See Notes 1(f) and 1(g) for further discussion of these charges.

(c) In 2009, the Company recorded $11 million in severance and other charges. The Company expects $4 million will be substantially

paid by the end of the first quarter of 2010, with the remaining balance scheduled for payment later in 2010. In 2008, the Company

recorded $9 million in severance charges as a result of its capacity reductions.

(d) In 2009, the Company incurred $6 million in costs related to its liquidity improvement program, which primarily consisted of

professional and legal fees.

(e) In 2008, in connection with the effort to consolidate functions and integrate the Company's organizations, procedures and

operations, the Company incurred $35 million of merger-related transition expenses. These

84