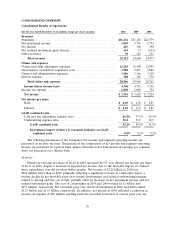

Travelers 2010 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2010 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

|

|

We are subject to regulation by some states as an insurance holding company system. Our

insurance subsidiaries are subject to various regulatory restrictions that limit the maximum amount of

dividends available to be paid to their parent without prior approval of insurance regulatory authorities.

In a time of prolonged economic downturn or otherwise, regulators may choose to further restrict the

ability of insurance subsidiaries to make payments to their parent companies. The ability of our

insurance subsidiaries to pay dividends to our holding company is also restricted by regulations that set

standards of solvency that must be met and maintained. The inability of our insurance subsidiaries to

pay dividends to our holding company in an amount sufficient to meet our debt service obligations and

other cash requirements could harm our ability to meet our obligations, to pay future shareholder

dividends and to make share repurchases.

Disruptions to our relationships with our independent agents and brokers could adversely affect

us. We market our insurance products primarily through independent agents and brokers. An

important part of our business is written through less than a dozen such intermediaries. Loss of all or a

substantial portion of the business provided through such agents and brokers could materially and

adversely affect our future business volume and results of operations. We may also seek to develop new

product distribution channels, including our current efforts to establish a direct-to-consumer platform in

the Personal Insurance segment. In addition, agents and brokers may create alternate distribution

channels for commercial business, such as insurance exchanges, that may adversely impact product

differentiation and pricing. Our or their efforts with respect to alternate distribution channels could

adversely impact our business relationship with independent agents and brokers who currently market

our products, resulting in a lower volume of business generated from these sources.

We rely on internet applications for the marketing and sale of certain of our products, and we may

increasingly rely on internet applications and toll-free numbers for distribution. In some instances, our

agents and brokers are required to access separate business platforms to execute the sale of our

personal insurance or commercial insurance products. Should internet disruptions occur, or frustration

with our business platforms or distribution initiatives develop among our independent agents and

brokers, the resulting loss of business could materially and adversely affect our future business volume

and results of operations.

Our efforts to develop new products or expand in targeted markets may not be successful and

may create enhanced risks. A number of our recent and planned business initiatives involve

developing new products or expanding existing products in targeted markets. This includes the

following efforts, from time to time, to protect or grow market share:

• We may develop products that insure risks we have not previously insured or contain new

coverage or coverage terms.

• We may refine our underwriting processes. For example, in certain of our businesses in recent

years, we have substantially increased the volume of business that flows through our automated

underwriting and pricing systems.

• We may seek to expand distribution channels, such as our efforts to develop a

direct-to-consumer platform in Personal Insurance.

• We may focus on geographic markets within or outside of the United States where we have had

relatively little or no market share.

We may not be successful in introducing new products or expanding in targeted markets and, even

if we are successful, these efforts may create enhanced risks. Among other risks:

• Demand for new products or in new markets may not meet our expectations.

• To the extent we are able to market new products or expand in new markets, our risk exposures

may change, and the data and models we use to manage such exposures may not be as

60