Travelers 2010 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2010 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

|

|

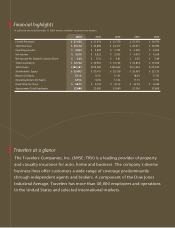

2010 ANNUAL REPORT 5

LETTER TO SHAREHOLDERS

While these are two very different ends of the spectrum,

we are positioning ourselves to execute in either environment,

as well as along the spectrum.

To position the company for a low-growth environment, we

continue to manage closely our cost structure at the same

time that we invest in our businesses to improve our effi ciency,

effectiveness and risk selection capabilities, with the

objective of reducing volatility in our results and improving

performance relative to the insurance industry broadly.

With respect to the second scenario, infl ation presents its own

challenges for property and casualty insurance companies.

Loss costs on existing claims tend to go up — potentially

more than is refl ected in our claim reserves. In addition,

interest rates tend to rise in this environment, positively

impacting investment yields but negatively impacting

the value of our existing investments in our fi xed income

portfolio. To address the possibility of infl ation, we have

further shortened the duration of our fi xed income

investment portfolio. In any event, we generally hold

our fi xed income investments to maturity and, to that

extent, temporary decreases in value of our fi xed maturity

investments should not become realized.

In either scenario, we believe that the creditworthiness of our fi xed

income portfolio is paramount, and we have adhered strictly to

our strategy of maintaining a high-quality investment portfolio.

Finally, our business depends to a signifi cant degree on our

relationships. When economic times are tough, relationships

are more important than ever. We continue to provide

responsive, caring and focused service to our agents and

brokers and to our policyholders. This dedication has been

rewarded through agent and customer loyalty and enhanced

reputation in the marketplace.

Commitment to community

As always, our commitment to the greater community

extends beyond selling insurance. In 2010, we provided

more than $21 million in community support in the

form of grants, sponsorships and other giving, including

through the Travelers Foundation. Our commitment and

our efforts related to education and career opportunities

Resseguros S.A., Brazil’s market leader in surety. This joint

venture provides a signifi cant opportunity for us to leverage

our leading U.S. surety franchise to enter the Brazilian

market and to do so with a local market leader. The joint

venture also provides an exceptional platform for expanding

beyond the surety business and into the growing property

and casualty market in Brazil. The transaction is expected to

close in the fi rst half of 2011.

• Personal Insurance — We continued to grow our Personal

Insurance business in 2010, which was quite an achievement

in a marketplace that is crowded with competitors and

advertising messages. Net written premiums for the year

were approximately $7.6 billion, a meaningful increase over

the prior year. We are very pleased with our performance

in both our agency auto and homeowners businesses,

where we added policies while achieving pricing gains.

Our success in these areas was due to several competitive

advantages, including our sophisticated pricing and risk

management, focused product delivery, superior claim

performance and strong agency relationships. In our new

direct-to-consumer business, we have made signifi cant

progress in our infrastructure and technology, positioning

us to offer auto and homeowners products and services to

those consumers who desire to do business directly with an

insurance company. Additionally, these improvements have

enhanced the services we provide to customers who come to

us through independent agents.

Looking ahead

As we enter 2011, we ask ourselves what the new year and

beyond will have in store for business in general, as well as for

the property and casualty industry and Travelers specifi cally.

We believe that, among others, two very different scenarios

are possible:

• The foreseeable future could present similar or even

more challenging conditions to those we are experiencing

today — high unemployment, low economic growth, low

investment returns and an insurance cycle with soft pricing.

• Alternatively, the foreseeable future could present a more

robust outlook, although potentially including infl ation.

* Total return to shareholders is measured as the change in stock price plus

the cumulative amount of dividends, assuming dividend reinvestment.

Total return to shareholders* from

January 1, 2005 to December 31, 2010

74.1%

Travelers has paid cash dividends without

interruption for 139 years.

139 years