Travelers 2010 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2010 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

|

|

wildfires, severe winter weather, floods, volcanic eruptions, theft, vandalism, fires, explosions, terrorism

and financial loss due to business interruption resulting from covered property damage. For additional

information on terrorism coverages, see ‘‘Reinsurance—Catastrophe Reinsurance—Terrorism Risk

Insurance Acts.’’ Property also includes specialized equipment insurance, which provides coverage for

loss or damage resulting from the mechanical breakdown of boilers and machinery, and ocean and

inland marine insurance, which provides coverage for goods in transit and unique, one-of-a-kind

exposures.

General Liability coverage insures businesses against third-party claims arising from accidents

occurring on their premises or arising out of their operations, including as a result of injuries sustained

from products sold. Specialized liability policies may also include coverage for directors’ and officers’

liability arising in their official capacities, employment practices liability insurance, fiduciary liability for

trustees and sponsors of pension, health and welfare, and other employee benefit plans, errors and

omissions insurance for employees, agents, professionals and others arising from acts or failures to act

under specified circumstances, as well as umbrella and excess insurance.

Commercial Multi-Peril provides a combination of the property and liability coverages described in

the foregoing product line descriptions.

Net Retention Policy

The following discussion reflects the Company’s retention policy with respect to the Business

Insurance segment as of January 1, 2011. For third-party liability, Business Insurance generally limits its

net retention, through the use of reinsurance, to a maximum of $18.8 million per insured, per

occurrence after the Company retains an aggregate layer of expected losses. The net retained amount

per risk for property exposures is generally limited to $17.0 million, after reinsurance. The Company

generally retains its workers’ compensation exposures. Reinsurance treaties often have aggregate limits

or caps which may result in larger net per-risk retentions if the aggregate limits or caps are reached.

The Company utilizes facultative reinsurance to provide additional limits capacity or to reduce

retentions on an individual risk basis. The Company may also retain amounts greater than those

described herein based upon the individual characteristics of the risk.

Geographic Distribution

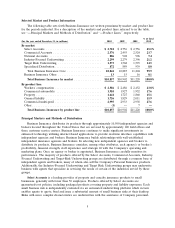

The following table shows the geographic distribution of Business Insurance’s direct written

premiums for the states that accounted for the majority of premium volume for the year ended

December 31, 2010:

% of

State Total

California .................................................. 13.2%

New York ................................................. 7.8

Texas ..................................................... 7.5

Illinois .................................................... 4.6

Florida ................................................... 4.3

Pennsylvania ................................................ 4.2

New Jersey ................................................ 3.6

Massachusetts .............................................. 3.5

All others(1) ............................................... 51.3

Total ................................................... 100.0%

(1) No other single state accounted for 3.0% or more of the total direct written premiums

written in 2010 by the Business Insurance segment.

8