Travelers 2010 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2010 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

|

|

loss amount in a one-year timeframe, not over a multi-year timeframe. Also, because the

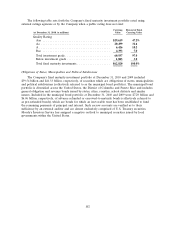

probabilities relate to a single event, the probabilities do not address the likelihood of

more than one event occurring in a particular period, and, therefore, the amounts do not

address potential aggregate catastrophe losses occurring in a one-year timeframe.

(2) The percentage of common equity is calculated by dividing (a) indicated loss amounts in

dollars by (b) total common equity excluding net unrealized investment gains and losses,

net of taxes. Net unrealized investment gains and losses can be significantly impacted by

both discretionary and other economic factors and are not necessarily indicative of

operating trends. Accordingly, in the opinion of the Company’s management, the

percentage of common equity calculated on this basis provides a useful metric for

investors to understand the potential impact of a single hurricane or single earthquake on

the Company’s financial position.

The threshold loss amounts in the tables above are net of reinsurance, after-tax and exclude most

loss adjustment expenses, which historically have been less than 10% of loss estimates. The amounts for

hurricanes reflect U.S. exposures and include property exposures, property residual market exposures

and an adjustment for certain non-property exposures. The amounts for earthquakes reflect U.S. and

Canadian exposures and include property exposures and workers’ compensation exposures. The

Company does not believe that the inclusion of hurricane or earthquake losses arising from other

geographical areas or other exposures would materially change the estimated threshold loss amounts.

This information in the tables is based on the Company’s in-force portfolio and catastrophic

reinsurance program as of December 31, 2010.

Catastrophe modeling relies upon inputs based on experience, science, engineering and history.

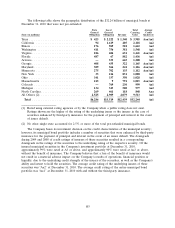

These inputs reflect a significant amount of judgment and are subject to changes which may result in

volatility in the modeled output. Catastrophe modeling output may also fail to account for risks that

are outside the range of normal probability or are otherwise unforeseeable. Catastrophe modeling

assumptions include, among others, the portion of purchased reinsurance that is collectible after a

catastrophic event, which may prove to be materially incorrect. Consequently, catastrophe modeling

estimates are subject to significant uncertainty. In the tables above, the uncertainty associated with the

estimated threshold loss amounts increases significantly as the likelihood of exceedance decreases. In

other words, in the case of a relatively more remote event (e.g., 1-in-1,000), the estimated threshold

loss amount is relatively less reliable. Actual losses from an event could materially exceed the indicated

threshold loss amount. In addition, more than one such event could occur in any period.

Moreover, the Company is exposed to the risk of material losses from other than property and

workers’ compensation coverages arising out of hurricanes and earthquakes, and it is exposed to

catastrophe losses from perils other than hurricanes and earthquakes, such as windstorms, hail,

wildfires, severe winter weather, floods, volcanic eruptions and acts of terrorism.

There are no industry-standard methodologies or assumptions for projecting catastrophe exposure.

Accordingly, catastrophe estimates provided by different insurers may not be comparable.

For more information about the Company’s exposure to catastrophe losses, see ‘‘Item 1A—Risk

Factors—Catastrophe losses could materially and adversely affect our results of operations, our

financial position and/or liquidity, and could adversely impact our ratings, our ability to raise capital

and the availability and cost of reinsurance.’’

CHANGING CLIMATE CONDITIONS

Severe weather events over the last several years have underscored the unpredictability of future

climate trends and created uncertainty regarding insurers’ exposures to financial loss as a result of

catastrophe and other weather-related events. Some scientists believe that, in recent years, changing

109