Travelers 2009 Annual Report Download - page 177

Download and view the complete annual report

Please find page 177 of the 2009 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

|

|

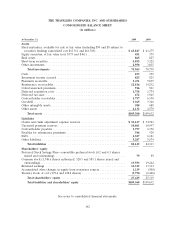

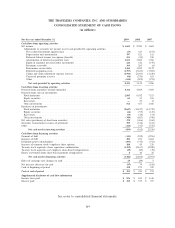

THE TRAVELERS COMPANIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The consolidated financial statements include the accounts of The Travelers Companies, Inc.

(together with its subsidiaries, the Company). The preparation of the consolidated financial statements

in conformity with U.S. generally accepted accounting principles (GAAP) requires management to

make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure

of contingent assets and liabilities at the date of the consolidated financial statements and the reported

amounts of revenues and claims and expenses during the reporting period. Actual results could differ

from those estimates. Certain reclassifications have been made to the 2008 and 2007 financial

statements to conform to the 2009 presentation. All material intercompany transactions and balances

have been eliminated.

Adoption of Accounting Standards Updates

Noncontrolling Interests in Consolidated Financial Statements

In December 2007, the FASB issued updated guidance that established accounting and reporting

standards for noncontrolling interests in a subsidiary and for the deconsolidation of a subsidiary. In

addition, the guidance clarified that a noncontrolling interest in a subsidiary is an ownership interest in

the consolidated entity that should be reported as a component of equity rather than a liability in the

consolidated financial statements.

The provisions of the guidance were effective on a prospective basis beginning January 1, 2009,

except for the presentation and disclosure requirements, which were applied on a retrospective basis for

all periods presented. The adoption of the guidance on January 1, 2009 did not have a material effect

on the Company’s results of operations, financial position or liquidity.

Determination of the Useful Life of Intangible Assets

In April 2008, the FASB issued updated guidance that amended the factors that an entity should

consider in determining the useful life of a recognized intangible asset to include the entity’s historical

experience in renewing or extending similar arrangements, whether or not the arrangements have

explicit renewal or extension provisions. Previously, an entity was precluded from using its own

assumptions about renewal or extension of an arrangement where there was likely to be substantial cost

or modifications. Entities without their own historical experience should consider the assumptions

market participants would use about renewal or extension. The guidance may result in the useful life of

an entity’s intangible asset differing from the period of expected cash flows that was used to measure

the fair value of the underlying asset. Disclosure of an entity’s intent and/or ability to renew or extend

the arrangement is also required.

The guidance was effective for financial statements issued for fiscal years beginning after

December 15, 2008 and for interim periods within those fiscal years. The adoption of the guidance on

January 1, 2009 did not have a material effect on the Company’s results of operations, financial

position or liquidity and did not require additional disclosures related to existing intangible assets.

Participating Securities Granted in Share-Based Payment Transactions

In June 2008, the FASB issued updated guidance that addressed whether instruments granted in

share-based payment transactions are participating securities prior to vesting and, therefore, should be

165