Travelers 2008 Annual Report Download - page 217

Download and view the complete annual report

Please find page 217 of the 2008 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

|

|

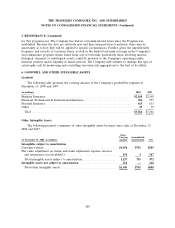

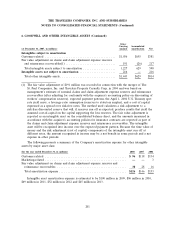

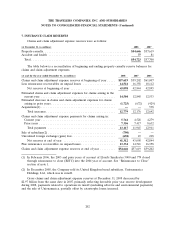

THE TRAVELERS COMPANIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

7. INSURANCE CLAIM RESERVES (Continued)

Personal Insurance. Net favorable prior year reserve development in 2007 totaled $152 million,

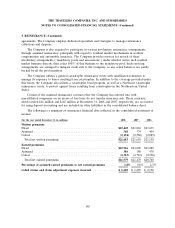

driven by better than expected automobile loss experience due in part to claim initiatives and fewer

than expected late reported homeowners’ claims related to non-catastrophe weather events that

occurred in the fourth quarter of 2006. In addition, a portion of net favorable prior year reserve

development in the Homeowners and Other line of business in 2007 was attributable to a decrease in

the number of claims due to changes in the marketplace, including higher deductibles and fewer small-

dollar claims.

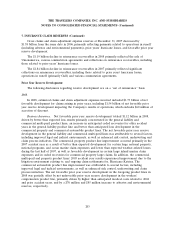

2006.

In 2006, estimated claims and claim adjustment expenses included $429 million of net favorable

development for claims arising in prior years, including $394 million of net favorable prior year reserve

development impacting the Company’s results of operations which excludes $62 million of accretion of

discount.

Business Insurance. Net favorable prior year reserve development totaled $21 million in 2006,

primarily concentrated in the commercial multi-peril, general liability, property and commercial

automobile lines of business, partially offset by increases for asbestos reserves and environmental

reserves (as discussed in more detail in the following ‘‘Asbestos and Environmental Reserves’’ section),

as well as reserve strengthening for assumed reinsurance business in runoff. The commercial multi-peril

and liability lines of business experienced better than anticipated loss development that was attributable

to several factors, including improving legal and judicial environments, as well as enhanced risk control,

underwriting and claim process initiatives. The favorable prior year reserve development in the property

line of business primarily reflected less ‘‘demand surge’’ inflation than originally estimated for 2005

accident year non-catastrophe related and catastrophe losses. ‘‘Demand surge’’ refers to significant

short-term increases in building material and labor costs due to a sharp increase in demand for those

materials and services. The commercial automobile line of business experienced better than expected

loss development which was attributable to improved legal and judicial environments, claim handling

initiatives focused on the automobile line of insurance and improvements in auto safety technology.

The reserve strengthening in assumed reinsurance was primarily due to changes in projected loss

development driven by an unanticipated change in the claim settlement patterns of the underlying

casualty exposures.

Financial, Professional & International Insurance. Net favorable prior year development in 2006

totaled $14 million.

Personal Insurance. Net favorable prior year reserve development in 2006 totaled $359 million,

driven by better than expected auto bodily injury loss experience and a decline in non-catastrophe

losses in the Homeowners and Other line of business, and a reduction in loss estimates for the 2005

hurricanes. In the Automobile line of business, the improvement was partially driven by better than

expected results from changes in claim handling practices. These changes included practices which have

allowed case reserves to be established more accurately earlier in the claim settlement process, thereby

changing historical loss development patterns. In addition, industry and Company initiatives to fight

fraud in several states led to a decrease in the total number of claims and a change in historical loss

development patterns. In the Homeowners and Other line of business, favorable prior year reserve

development was partially driven by a significant decrease in the number of claims, attributable to

changes in the marketplace, including higher deductibles and fewer small-dollar claims. These changes

also resulted in a change in historical loss development patterns. In addition, non-catastrophe

205