Metro PCS 2008 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2008 Metro PCS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

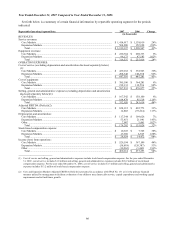

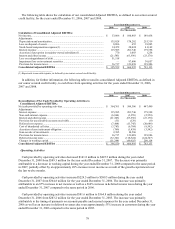

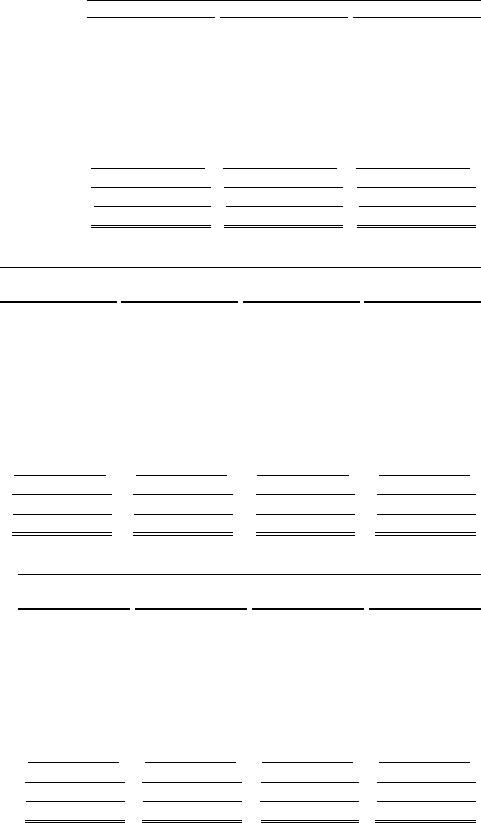

75

CPGA — We utilize CPGA to assess the efficiency of our distribution strategy, validate the initial capital

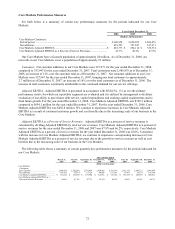

invested in our customers and determine the number of months to recover our customer acquisition costs. This

measure also allows us to compare our average acquisition costs per new customer to those of other wireless

broadband mobile providers. Equipment revenues related to new customers are deducted from selling expenses in

this calculation as they represent amounts paid by customers at the time their service is activated that reduce our

acquisition cost of those customers. Additionally, equipment costs associated with existing customers, net of related

revenues, are excluded as this measure is intended to reflect only the acquisition costs related to new customers.

The following table reconciles total costs used in the calculation of CPGA to selling expenses, which we consider to

be the most directly comparable GAAP financial measure to CPGA.

Year Ended December 31,

2006 2007 2008

(In thousands, except gross customer additions and

CPGA)

Calculation of Cost Per Gross Addition (CPGA):

Selling expenses .........................................................................................

.

$ 104,620 $ 153,065 $ 212,293

Less: Equipment revenues .......................................................................

.

(255,916) (316,537) (314,266)

Add: Equipment revenue not associated with new customers .................

.

114,392 142,822 149,029

Add: Cost of equipment...........................................................................

.

476,877 597,233 704,648

Less: Equipment costs not associated with new customers .....................

.

(155,930) (192,153) (244,311)

Gross addition expenses..............................................................................

.

$ 284,043 $ 384,430 $ 507,393

Divided by: Gross customer additions........................................................

.

2,345,135 3,004,177 3,988,692

CPGA .........................................................................................................

.

$ 121.12 $ 127.97 $ 127.21

Three Months Ended

March 31,

2007

June 30,

2007

September 30,

2007

December 31,

2007

(In thousands, except gross customer additions and CPGA)

Calculation of Cost Per Gross Addition (CPGA):

Selling expenses ...................................................................... $ 30,106 $ 33,365 $ 35,625 $ 53,969

Less: Equipment revenues .................................................... (97,170) (71,835) (67,607) (79,925)

Add: Equipment revenue not associated with new

customers............................................................................ 42,009 33,892 31,590 35,330

Add: Cost of equipment........................................................ 173,308 133,439 131,179 159,308

Less: Equipment costs not associated with new

customers............................................................................ (55,169) (43,795) (43,254) (49,936)

Gross addition expenses........................................................... $ 93,084 $ 85,066 $ 87,533 $ 118,746

Divided by: Gross customer additions..................................... 832,983 660,149 671,379 839,666

CPGA ...................................................................................... $ 111.75 $ 128.86 $ 130.38 $ 141.42

Three Months Ended

March 31,

2008

June 30,

2008

September 30,

2008

December 31,

2008

(In thousands, except gross customer additions and CPGA)

Calculation of Cost Per Gross Addition (CPGA):

Selling expenses .......................................................................... $ 46,647 $ 53,180 $ 58,916 $ 53,551

Less: Equipment revenues ........................................................ (100,384) (80,245) (76,030) (57,606)

Add: Equipment revenue not associated with new

customers................................................................................ 45,803 37,613 33,295 32,318

Add: Cost of equipment............................................................ 200,158 160,088 160,538 183,864

Less: Equipment costs not associated with new customers ...... (72,212) (58,993) (56,891) (56,215)

Gross addition expenses............................................................... $ 120,012 $ 111,643 $ 119,828 $ 155,912

Divided by: Gross customer additions......................................... 960,083 792,823 934,607 1,301,179

CPGA .......................................................................................... $ 125.00 $ 140.82 $ 128.21 $ 119.82

CPU — CPU is cost of service and general and administrative costs (excluding applicable non-cash stock-based

compensation expense included in cost of service and general and administrative expenses) plus net loss on

equipment transactions unrelated to initial customer acquisition exclusive of pass through charges, divided by the

sum of the average monthly number of customers during such period. CPU does not include any depreciation and

amortization expense. Management uses CPU as a tool to evaluate the non-selling cash expenses associated with

ongoing business operations on a per customer basis, to track changes in these non-selling cash costs over time, and

to help evaluate how changes in our business operations affect non-selling cash costs per customer. In addition, CPU

provides management with a useful measure to compare our non-selling cash costs per customer with those of other

wireless providers. We believe investors use CPU primarily as a tool to track changes in our non-selling cash costs

over time and to compare our non-selling cash costs to those of other wireless providers, although other wireless

carriers may calculate this measure differently. The following table reconciles total costs used in the calculation of