Metro PCS 2008 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2008 Metro PCS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

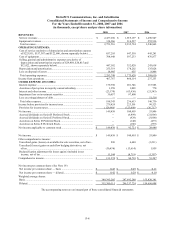

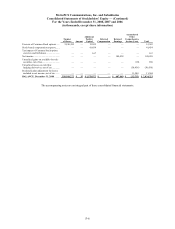

MetroPCS Communications, Inc. and Subsidiaries

Notes to Consolidated Financial Statements

December 31, 2008, 2007 and 2006

F-9

Operating Segments

SFAS No. 131 “Disclosure About Segments of an Enterprise and Related Information,” (“SFAS No. 131”),

establishes standards for the way that public business enterprises report information about operating segments in

annual financial statements. At December 31, 2008, the Company had thirteen operating segments based on

geographic regions within the United States: Atlanta, Boston, Dallas/Ft. Worth, Detroit, Las Vegas, Los Angeles,

Miami, New York, Orlando/Jacksonville, Philadelphia, San Francisco, Sacramento and Tampa/Sarasota. The

Company aggregates its operating segments into two reportable segments: Core Markets and Expansion Markets

(See Note 20).

Use of Estimates in Financial Statements

The preparation of financial statements in conformity with accounting principles generally accepted in the United

States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported

amounts of certain assets and liabilities and disclosure of contingent liabilities at the date of the financial statements

and the reported amounts of expenses during the reporting period. Actual results could differ from those estimates.

The most significant of such estimates used by the Company include:

• allowance for uncollectible accounts receivable;

• valuation of inventories;

• valuation of investment securities;

• estimated useful life of assets;

• accrued property, plant and equipment for the percentage of construction services received;

• impairment of long-lived assets and indefinite-lived assets;

• likelihood of realizing benefits associated with temporary differences giving rise to deferred tax assets;

• reserves for uncertain tax positions;

• estimated customer life in terms of amortization of certain deferred revenue;

• valuation of common stock prior to the Offering; and

• stock-based compensation expense.

Derivative Instruments and Hedging Activities

The Company accounts for its hedging activities under SFAS No. 133, “Accounting for Derivative Instruments

and Hedging Activities,” as amended (“SFAS No. 133”). The standard requires the Company to recognize all

derivatives on the consolidated balance sheet at fair value. Changes in the fair value of derivatives are to be recorded

each period in earnings or on the accompanying consolidated balance sheets in accumulated other comprehensive

income (loss) depending on the type of hedged transaction and whether the derivative is designated and effective as

part of a hedged transaction. Gains or losses on derivative instruments reported in accumulated other comprehensive

income (loss) must be reclassified to earnings in the period in which earnings are affected by the underlying hedged

transaction and the ineffective portion of all hedges must be recognized in earnings in the current period. The

Company’s use of derivative financial instruments is discussed in Note 6.