Metro PCS 2008 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2008 Metro PCS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

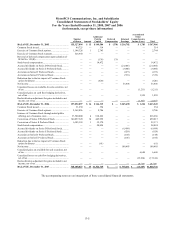

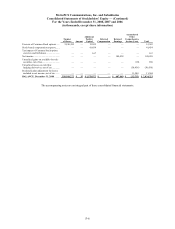

|

|

MetroPCS Communications, Inc. and Subsidiaries

Notes to Consolidated Financial Statements

December 31, 2008, 2007 and 2006

F-15

Recent Accounting Pronouncements

In December 2007, the FASB issued SFAS No. 141(R), “Business Combinations,” (“SFAS No. 141(R)”), which

establishes principles and requirements for how an acquirer recognizes and measures in its financial statements the

identifiable assets acquired, the liabilities assumed, any noncontrolling interest in the acquiree and the goodwill

acquired. SFAS No. 141(R) also establishes disclosure requirements to enable the evaluation of the nature and

financial effects of the business combination. SFAS No. 141(R) is effective for financial statements issued for fiscal

years beginning after December 15, 2008 and early adoption is prohibited. The implementation of this standard did

not have a material impact on the Company’s financial condition or results of operations.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial

Statements,” (“SFAS No. 160”), which establishes accounting and reporting standards for ownership interests in

subsidiaries held by parties other than the parent, the amount of consolidated net income attributable to the parent

and to the noncontrolling interest, changes in a parent’s ownership interest, and the valuation of retained

noncontrolling equity investments when a subsidiary is deconsolidated. SFAS No. 160 also establishes disclosure

requirements that clearly identify and distinguish between the interests of the parent and the interests of the

noncontrolling owners. SFAS No. 160 is effective for financial statements issued for fiscal years beginning after

December 15, 2008 and early adoption is prohibited. The implementation of this standard did not have a material

impact on the Company’s financial condition or results of operations.

In March 2008, the FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging

Activities, an amendment of FASB Statement No. 133,” (“SFAS No. 161”). SFAS No. 161 requires enhanced

disclosures about a company’s derivative and hedging activities. These enhanced disclosures will discuss (a) how

and why a company uses derivative instruments, (b) how derivative instruments and related hedged items are

accounted for under FASB Statement No. 133 and its related interpretations and (c) how derivative instruments and

related hedged items affect a company’s financial position, results of operations and cash flows. SFAS No. 161 is

effective for fiscal years beginning on or after November 15, 2008, with earlier adoption allowed. The

implementation of this standard did not have a material impact on the Company’s financial condition or results of

operations.

In April 2008, the FASB issued FSP SFAS No. 142-3, “Determination of the Useful Life of Intangible Assets,”

(“FSP SFAS No. 142-3”). FSP SFAS No. 142-3 amends the factors that should be considered in developing renewal

or extension assumptions used to determine the useful life of a recognized intangible asset under SFAS No. 142,

“Goodwill and Other Intangible Assets.” FSP SFAS No. 142-3 is effective for fiscal years beginning after

December 15, 2008. The implementation of this standard did not have a material impact on the Company’s

financial condition or results of operations.

In October 2008, the FASB issued FSP SFAS No. 157-3 “Determining Fair Value of a Financial Asset in a

Market That Is Not Active,” (“FSP SFAS No. 157-3”). FSP SFAS No. 157-3 clarified the application of SFAS No.

157 in an inactive market. It demonstrates how the fair value of a financial asset is determined when the market for

that financial asset is inactive. FSP SFAS No. 157-3 was effective upon issuance, including prior periods for which

financial statements had not been issued. The implementation of this standard did not have a material impact on the

Company’s financial condition or results of operations.

In November 2008, the FASB issued EITF No. 08-6, “Equity Method Investment Accounting Considerations,”

(“EITF No. 08-6”). EITF 08-6 clarifies the accounting treatment for certain transactions and impairment

considerations involving equity method investments. EITF No. 08-6 is effective for fiscal years and interim periods

beginning on or after December 15, 2008, consistent with the effective dates of SFAS No. 141(R) and SFAS No.

160. The implementation of this standard did not have a material impact on the Company’s financial condition or

results of operations.