LensCrafters 2013 Annual Report Download - page 184

Download and view the complete annual report

Please find page 184 of the 2013 LensCrafters annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

|

|

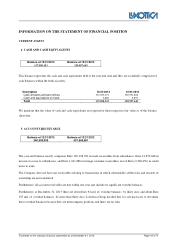

Footnotes to the statutory financial statements as of December 31, 2013 Page 17 of 71

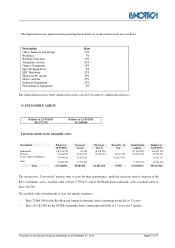

3. ESTIMATES AND ASSUMPTIONS

Use of estimates. The preparation of financial statements in conformity with IFRS requires management to make

estimates and assumptions that influence the value of assets and liabilities reported in the statement of financial

position as well as revenues and costs reported in the statement of income, and also the disclosures included in the

notes to the financial statements in relation to contingent assets and liabilities as of the date the financial statements

were authorized for issue. Significant judgment and estimates are required in the determination of allowances against

receivables, inventories and deferred tax assets, in the calculation of pension and other long-term employee benefits,

legal and other provisions for contingent liabilities and in the determination of the value of long-lived assets, including

goodwill.

Estimates are based on past experience and other relevant factors. Actual results could therefore differ from those

estimates. Accounting estimates are periodically reviewed and the effects of any change are reflected in profit or loss

in the period the change occurs.

The current ongoing economic and financial crisis has made it necessary to make assumptions of a highly uncertain

nature about future performance, meaning that actual results in the next year may differ from estimates and could

require potentially material adjustments to the carrying amount of the related items, the size of which clearly cannot

be estimated or forecast at present.

The most significant accounting policies requiring greater judgment on the part of management when making

estimates are briefly described below.

• Valuation of inventories. Inventories that are obsolete and slow-moving are regularly reviewed and written down

if their recoverable amount is lower than their carrying amount. Write-downs are calculated on the basis of

management assumptions and estimates, derived from experience and past results;

• Assessment of the recoverability of deferred tax assets. The valuation of deferred tax assets is based on forecast

income in future years, which depends on factors that could vary over time and could have significant effects on

the valuation of deferred tax assets;

• Income taxes. The determination of the Company's tax liabilities requires the use of judgment by management

with respect to transactions whose tax implications are not certain at the end of the reporting period. The Company

recognizes liabilities that may arise from future inspections by the tax authorities, based on an estimate of the taxes

expected to be paid. If the outcome of such inspections should differ from that estimated by management, there

could be significant effects on both current and deferred taxes;

• Valuation of investments. The value of investments is tested for impairment if any of the trigger events envisaged

by IAS 36 occurs. This test requires management to make subjective judgments based on information available

within the Group and on the market, as well as past experience;

• Pension plans. The present value of the pension liabilities depends on a number of factors that are determined

using actuarial techniques based on certain assumptions. These assumptions relate to the discount rate, the

expected return on plan assets, the rate of future salary increases, and mortality and resignation rates. Any change

in these assumptions could have significant effects on pension liabilities.