LensCrafters 2013 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2013 LensCrafters annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

|

|

3. FINANCIAL RISKS

The assets of the Group are exposed to different types of financial risk: market risk (which includes exchange

rate risks, interest rate risk relative to fair value variability and cash flow uncertainty), credit risk and liquidity risk. The

risk management strategy of the Group aims to stabilize the results of the Group by minimizing the potential effects due

to volatility in financial markets. The Group uses derivative financial instruments, principally interest rate and currency

swap agreements, as part of its risk management strategy.

Financial risk management is centralized within the Treasury department which identifies, evaluates and

implements financial risk hedging activities, in compliance with the Financial Risk Management Policy guidelines

approved by the Board of Directors, and in accordance with the Group operational units. The Policy defines the

guidelines for any kind of risk, such as the exchange rate risk, the interest rate risk, credit risk and the utilization of

derivative and non-derivative instruments. The Policy also specifies the management activities, the permitted

instruments, the limits and proxies for responsibilities.

(a) Exchange rate risk

The Group operates at the international level and is therefore exposed to exchange rate risk related to the

various currencies with which the Group operates. The Group only manages transaction risk. The transaction exchange

rate risk derives from commercial and financial transactions in currencies other than the functional currency of the

Group, i.e., the Euro.

The primary exchange rate to which the Group is exposed is the Euro/USD exchange rate.

The exchange rate risk management policy defined by the Group’s management states that transaction

exchange rate risk must be hedged for a percentage between 50% and 100% by trading forward currency contracts or

permitted option structures with third parties.

This exchange rate risk management policy is applied to all subsidiaries, including companies which have been

recently acquired.

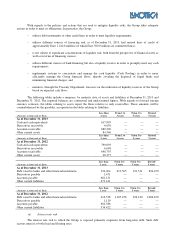

If the Euro/USD exchange rate increases by 10% as compared to the actual 2013 and 2012 average exchange

rates and all other variables remain constant, the impact on net income and equity would have been a decrease of

Euro 72.8 million and Euro 56.7 million, in 2013 and 2012, respectively. If the Euro/USD exchange rate decreases by

10% as compared to the actual 2013 and 2012 average exchange rates and all other variables remain constant, the

impact on net income and equity would have been an increase of Euro 89.0 million and Euro 69.3 million in 2013 and

2012, respectively. Even if exchange rate derivative contracts are stipulated to hedge future commercial transactions as

well as assets and liabilities previously recorded in the financial statements in foreign currency, these contracts, for

accounting purposes, may not be accounted for as hedging instruments.

(b) Price risk

The Group is generally exposed to price risk associated with investments in bond securities which are

classified as assets at fair value through profit and loss. As of December 31, 2013 and 2012, the Group investment

portfolio was fully divested. As a result, there was no exposure to price risk on such dates.

(c) Credit risk

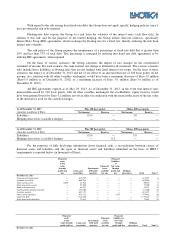

Credit risk exists in relation to accounts receivable, cash, financial instruments and deposits in banks and other

financial institutions.

c1) The credit risk related to commercial counterparties is locally managed and monitored by a group credit

control department for all entities included in the Wholesale distribution segment. Credit risk which originates within

the retail segment is locally managed by the companies included in the retail segment.

Losses on receivables are recorded in the financial statements if there are indicators that a specific risk exists

or as soon as risks of potential insolvency arise, by determining an adequate accrual for doubtful accounts.

The allowance for doubtful accounts used for the Wholesale segment and in accordance with the credit policy

of the Group is determined by assigning a rating to customers according to the following categories: