HTC 2013 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2013 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

|

|

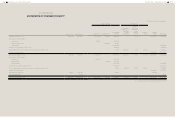

FINANCIAL INFORMATION FINANCIAL INFORMATION

198 199

Pension cost for an interim period is calculated

on a year-to-date basis by using the actuarially

determined pension cost rate at the end of the

prior financial year, adjusted for significant market

fluctuations since that time and for significant

curtailments, settlements, or other significant one-

time events.'

Share-based Payment Arrangements

Share-based payment transactions of the Company

Equity-settled share-based payments to employees

are measured at the fair value of the equity

instruments at the grant date.

The fair value determined at the grant date of the

equity-settled share-based payments is expensed on

a straight-line basis over the vesting period, based

on the Company's estimate of equity instruments

that will eventually vest, with a corresponding

increase in capital surplus - employee share options.

The fair value determined at the grant date of the

equity-settled share-based payments is recognized

as an expense in full at the grant date when the

share options granted vest immediately.

At the end of each reporting period, the Company

revises its estimate of the number of equity

instruments expected to vest. The impact of the

revision of the original estimates, if any, is recognized

in profit or loss such that the cumulative expense

reflects the revised estimate, with a corresponding

adjustment to the capital surplus - employee share

options.

Taxation

Income tax expense represents the sum of the tax

currently payable and deferred tax.

a. Current tax

According to the Income Tax Law, an additional tax

at 10% of unappropriated earnings is provided for

as income tax in the year the stockholders approve

to retain the earnings.

reduced to the extent that it is no longer probable

that sufficient taxable profits will be available to

allow all or part of the asset to be recovered. A

previously unrecognized deferred tax asset is also

reviewed at the end of each reporting period and

recognized to the to the extent that it has become

probable that future taxable profit will allow the

deferred tax asset to be recovered.

Deferred tax liabilities and assets are measured

at the tax rates that are expected to apply in the

period in which the liability is settled or the asset

realized, based on tax rates (and tax laws) that

have been enacted or substantively enacted by

the end of the reporting period. The measurement

of deferred tax liabilities and assets reflects the tax

consequences that would follow from the manner

in which the Company expects, at the end of the

reporting period, to recover or settle the carrying

amount of its assets and liabilities.

c. Current and deferred tax for the year

Current and deferred tax are recognized in profit

or loss, except when they relate to items that

are recognized in other comprehensive income

or directly in equity, in which case, the current

and deferred tax are also recognized in other

comprehensive income or directly in equity

respectively. Where current tax or deferred tax

arises from the initial accounting for a business

combination, the tax effect is included in the

accounting for the business combination.

Accrued Marketing Expenses

The Company accrues marketing expenses on the

basis of agreements and any known factors that

would significantly affect the accruals. In addition,

depending on the nature of relevant events, the

accrued marketing expenses are accounted for as an

increase in marketing expenses or as a decrease in

revenues.

Adjustments of prior years' tax liabilities are

added to or deducted from the current year's tax

provision.

b.Deferred tax

Deferred tax is recognized on temporary

differences between the carrying amounts of

assets and liabilities in the parent company only

financial statements and the corresponding tax

bases used in the computation of taxable profit.

Deferred tax liabilities are generally recognized for

all taxable temporary differences. Deferred tax

assets are generally recognized for all deductible

temporary differences, unused loss carry forward

and unused tax credits for purchases of machinery,

equipment and technology, research and

development expenditures, and personnel training

expenditures to the extent that it is probable that

taxable profits will be available against which

those deductible temporary differences can be

utilized. Such deferred tax assets and liabilities are

not recognized if the temporary difference arises

from goodwill or from the initial recognition (other

than in a business combination) of other assets

and liabilities in a transaction that affects neither

the taxable profit nor the accounting profit.

Deferred tax liabilities are recognized for taxable

temporary differences associated with investments

in subsidiaries and associates, and interests in joint

ventures, except where the Company is able to

control the reversal of the temporary difference

and it is probable that the temporary difference

will not reverse in the foreseeable future. Deferred

tax assets arising from deductible temporary

differences associated with such investments and

interests are only recognized to the extent that

it is probable that there will be sufficient taxable

profits against which to utilize the benefits of the

temporary differences and they are expected to

reverse in the foreseeable future.

The carrying amount of deferred tax assets is

reviewed at the end of each reporting period and

Treasury Stock

When the Company acquires its outstanding shares

that have not been disposed or retired, treasury

stock is stated at cost and shown as a deduction

in stockholders' equity. When treasury shares are

sold, if the selling price is above the book value, the

difference should be credited to the capital surplus

- treasury stock transactions. If the selling price is

below the book value, the difference should first be

offset against capital surplus from the same class

of treasury stock transactions, and the remainder, if

any, debited to retained earnings. The carrying value

of treasury stock is calculated using the weighted-

average approach in accordance with the purpose of

the acquisition.

When the Company's treasury stock is retired, the

treasury stock account should be credited, and

the capital surplus - premium on stock account

and capital stock account should be debited

proportionately according to the share ratio. The

carrying value of treasury stock in excess of the sum

of its par value and premium on stock should first be

offset against capital surplus from the same class of

treasury stock transactions, and the remainder, if any,

debited to retained earnings. The sum of the par

value and premium on treasury stock in excess of its

carrying value should be credited to capital surplus

from the same class of treasury stock transactions.

5. CRITICAL ACCOUNTING

JUDGEMENTS AND KEY

SOURCES OF ESTIMATION

UNCERTAINTY

In the application of the Company's accounting

policies, which are described in Note 4, the

management is required to make judgments,

estimates and assumptions about the carrying

amounts of assets and liabilities that are not readily

apparent from other sources. The estimates and

associated assumptions are based on historical

experience and other factors that are considered

to be relevant. Actual results may differ from these

estimates.