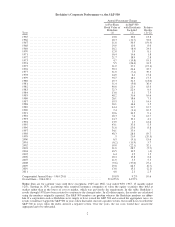

Berkshire Hathaway 2011 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2011 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

Let’s use IBM as an example. As all business observers know, CEOs Lou Gerstner and Sam Palmisano

did a superb job in moving IBM from near-bankruptcy twenty years ago to its prominence today. Their

operational accomplishments were truly extraordinary.

But their financial management was equally brilliant, particularly in recent years as the company’s

financial flexibility improved. Indeed, I can think of no major company that has had better financial management, a

skill that has materially increased the gains enjoyed by IBM shareholders. The company has used debt wisely, made

value-adding acquisitions almost exclusively for cash and aggressively repurchased its own stock.

Today, IBM has 1.16 billion shares outstanding, of which we own about 63.9 million or 5.5%.

Naturally, what happens to the company’s earnings over the next five years is of enormous importance to us.

Beyond that, the company will likely spend $50 billion or so in those years to repurchase shares. Our quiz for the

day: What should a long-term shareholder, such as Berkshire, cheer for during that period?

I won’t keep you in suspense. We should wish for IBM’s stock price to languish throughout the five years.

Let’s do the math. If IBM’s stock price averages, say, $200 during the period, the company will acquire

250 million shares for its $50 billion. There would consequently be 910 million shares outstanding, and we

would own about 7% of the company. If the stock conversely sells for an average of $300 during the five-year

period, IBM will acquire only 167 million shares. That would leave about 990 million shares outstanding after

five years, of which we would own 6.5%.

If IBM were to earn, say, $20 billion in the fifth year, our share of those earnings would be a full $100

million greater under the “disappointing” scenario of a lower stock price than they would have been at the higher

price. At some later point our shares would be worth perhaps $1

1

⁄

2

billion more than if the “high-price”

repurchase scenario had taken place.

The logic is simple: If you are going to be a net buyer of stocks in the future, either directly with your own

money or indirectly (through your ownership of a company that is repurchasing shares), you are hurt when stocks

rise. You benefit when stocks swoon. Emotions, however, too often complicate the matter: Most people, including

those who will be net buyers in the future, take comfort in seeing stock prices advance. These shareholders resemble

a commuter who rejoices after the price of gas increases, simply because his tank contains a day’s supply.

Charlie and I don’t expect to win many of you over to our way of thinking – we’ve observed enough

human behavior to know the futility of that – but we do want you to be aware of our personal calculus. And here

a confession is in order: In my early days I, too, rejoiced when the market rose. Then I read Chapter Eight of Ben

Graham’s The Intelligent Investor, the chapter dealing with how investors should view fluctuations in stock

prices. Immediately the scales fell from my eyes, and low prices became my friend. Picking up that book was one

of the luckiest moments in my life.

In the end, the success of our IBM investment will be determined primarily by its future earnings. But

an important secondary factor will be how many shares the company purchases with the substantial sums it is

likely to devote to this activity. And if repurchases ever reduce the IBM shares outstanding to 63.9 million, I will

abandon my famed frugality and give Berkshire employees a paid holiday.

************

Now, let’s examine the four major sectors of our operations. Each has vastly different balance sheet

and income characteristics from the others. Lumping them together therefore impedes analysis. So we’ll present

them as four separate businesses, which is how Charlie and I view them. Because we may be repurchasing

Berkshire shares from some of you, we will offer our thoughts in each section as to how intrinsic value compares

to carrying value.

7