Berkshire Hathaway 2011 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2011 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

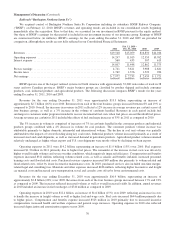

Management’s Discussion (Continued)

Investment and Derivative Gains/Losses (Continued)

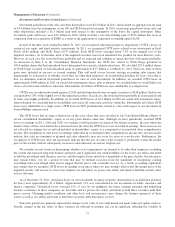

Investment gains/losses from sales and other dispositions were $2.2 billion in 2011 and included an aggregate pre-tax gain

of $1.8 billion from the redemptions of our GS and GE Preferred investments. In 2010, investment gains/losses from sales and

other dispositions included a $1.3 billion gain with respect to the redemption of the Swiss Re capital instrument. Other

investment gains and losses were $1.0 billion in 2010, which included a one-time holding gain of $979 million that arose in

connection with our acquisition of BNSF as a result of the application of acquisition accounting under GAAP.

In each of the three years ending December 31, 2011, we recognized other-than-temporary impairment (“OTTI”) losses on

certain of our equity and fixed maturity investments. In 2011, we recognized OTTI losses related to our investments in Kraft

Foods ($169 million) and Wells Fargo ($337 million). Such OTTI losses averaged about 7.5% of the original cost of the

impaired securities. As of that time, most of the impaired securities were in an unrealized loss position for more than two years.

However, in each case, the issuer had been profitable and we expected and continue to expect that they will remain profitable.

As discussed in Note 6 to the Consolidated Financial Statements, the OTTI loss related to Wells Fargo pertained to

103.6 million shares that had unrealized losses determined on a specific identification basis. We also held 255.4 million shares

of Wells Fargo in which we had unrealized gains of approximately $3.7 billion as of March 31, 2011. However, none of these

gains were included in our past or current earnings. This odd result occurs because existing accounting rules require that

impairments be evaluated as to whether or not they are other than temporary on an individual purchase lot basis, since that is

how we determine realized investment gains/losses on sales of such investments. In addition, we recorded OTTI losses of

approximately $400 million in 2011 on certain debt instruments where, after evaluation, we concluded that we would likely not

receive all contractual cash flows when due. Substantially all of these OTTI losses were attributable to a single issuer.

OTTI losses recorded in the fourth quarter of 2010 included unrealized losses on equity securities of $938 million. Such losses

averaged about 20% of the original cost of the impaired securities. In each case, the issuer had been profitable in recent periods and

in some cases highly profitable. In addition, we recorded OTTI losses of $1.0 billion in 2010 on certain debt instruments where,

after evaluation, we concluded that we would likely not receive all contractual cash flows when due. Substantially all of these OTTI

losses were attributable to a single issuer. OTTI losses in 2009 predominantly related to a loss with respect to our investment in

ConocoPhillips common stock.

The OTTI losses had no impact whatsoever on the asset values that were recorded in our Consolidated Balance Sheets or

on our consolidated shareholders’ equity as of any given balance sheet date. Although we have periodically recorded OTTI

losses in earnings in 2011, 2010 and 2009, we continue to hold positions in certain of the related securities. In cases where the

market values of these investments have increased since the dates the OTTI losses were recorded in earnings, these increases are

not reflected in earnings but are instead included in shareholders’ equity as a component of accumulated other comprehensive

income. The recognition of such losses in earnings rather than in accumulated other comprehensive income does not necessarily

indicate that sales are imminent or planned and sales ultimately may not occur for years or even decades. Furthermore, the

recognition of OTTI losses does not necessarily indicate that the loss in value of the security is permanent or that the market

price of the security will not subsequently increase to and ultimately exceed our original cost.

We consider several factors in determining whether or not impairments are deemed to be other than temporary, including

the current and expected long-term business prospects and if applicable, the creditworthiness of the issuer, our ability and intent

to hold the investment until the price recovers and the length of time and relative magnitude of the price decline. Security prices

may remain below cost for a period of time that may be deemed excessive from the standpoint of interpreting existing

accounting rules even though other factors suggest that the prices will eventually recover. As a result, accounting regulations

may require that we recognize OTTI losses in earnings in instances where we may strongly believe that the market price of the

impaired security will recover to at least our original cost and where we possess the ability and intent to hold the security until,

at least, that time.

As of December 31, 2011, unrealized losses on our investments in equity securities (determined on an individual purchase

lot basis) were approximately $1.4 billion. Approximately 91% was concentrated in our investments in banks, insurance and

finance companies. Unrealized losses averaged 12% of cost. In our judgment, the future earnings potential and underlying

business economics of these companies are favorable and we possess the ability and intent to hold these securities until their

prices recover. Changing market conditions and other facts and circumstances may change the business prospects of these

issuers as well as our ability and intent to hold these securities until their prices recover.

Derivative gains/losses primarily represent the changes in fair value of our credit default and equity index put option contracts.

Periodic changes in the fair values of these contracts are reflected in earnings and can be significant, reflecting the volatility of

77