Berkshire Hathaway 2011 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2011 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

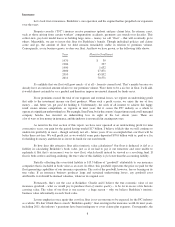

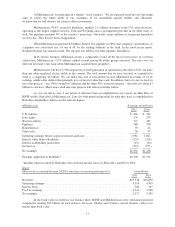

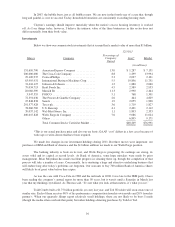

At yearend, we acquired Princeton Insurance, a New Jersey writer of medical malpractice policies. This

bolt-on transaction expands the managerial domain of Tim Kenesey, the star CEO of Medical Protective, our

Indiana-based med-mal insurer. Princeton brings with it more than $600 million of float, an amount that is

included in the following table.

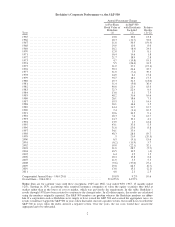

Here is the record of all four segments of our property-casualty and life insurance businesses:

Underwriting Profit Yearend Float

(in millions)

Insurance Operations 2011 2010 2011 2010

BH Reinsurance ................ $(714) $ 176 $33,728 $30,370

General Re .................... 144 452 19,714 20,049

GEICO ....................... 576 1,117 11,169 10,272

Other Primary .................. 242 268 5,960 5,141

$ 248 $2,013 $70,571 $65,832

Among large insurance operations, Berkshire’s impresses me as the best in the world.

Regulated, Capital-Intensive Businesses

We have two very large businesses, BNSF and MidAmerican Energy, that have important common

characteristics distinguishing them from our many other businesses. Consequently, we assign them their own sector

in this letter and also split out their combined financial statistics in our GAAP balance sheet and income statement.

A key characteristic of both companies is the huge investment they have in very long-lived, regulated

assets, with these partially funded by large amounts of long-term debt that is not guaranteed by Berkshire. Our

credit is not needed: Both businesses have earning power that even under terrible business conditions amply

covers their interest requirements. In a less than robust economy during 2011, for example, BNSF’s interest

coverage was 9.5x. At MidAmerican, meanwhile, two key factors ensure its ability to service debt under all

circumstances: The stability of earnings that is inherent in our exclusively offering an essential service and a

diversity of earnings streams, which shield it from the actions of any single regulatory body.

Measured by ton-miles, rail moves 42% of America’s inter-city freight, and BNSF moves more than

any other railroad – about 37% of the industry total. A little math will tell you that about 15% of all inter-city

ton-miles of freight in the U.S. is transported by BNSF. It is no exaggeration to characterize railroads as the

circulatory system of our economy. Your railroad is the largest artery.

All of this places a huge responsibility on us. We must, without fail, maintain and improve our 23,000

miles of track along with 13,000 bridges, 80 tunnels, 6,900 locomotives and 78,600 freight cars. This job requires

us to have ample financial resources under all economic scenarios and to have the human talent that can instantly

and effectively deal with the vicissitudes of nature, such as the widespread flooding BNSF labored under last

summer.

To fulfill its societal obligation, BNSF regularly invests far more than its depreciation charge, with the

excess amounting to $1.8 billion in 2011. The three other major U.S. railroads are making similar outlays.

Though many people decry our country’s inadequate infrastructure spending, that criticism cannot be levied

against the railroad industry. It is pouring money – funds from the private sector – into the investment projects

needed to provide better and more extensive service in the future. If railroads were not making these huge

expenditures, our country’s publicly-financed highway system would face even greater congestion and

maintenance problems than exist today.

Massive investments of the sort that BNSF is making would be foolish if it could not earn appropriate

returns on the incremental sums it commits. But I am confident it will do so because of the value it delivers.

Many years ago Ben Franklin counseled, “Keep thy shop, and thy shop will keep thee.” Translating this to our

regulated businesses, he might today say, “Take care of your customer, and the regulator – your customer’s

representative – will take care of you.” Good behavior by each party begets good behavior in return.

10