BMW 2011 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2011 BMW annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

|

|

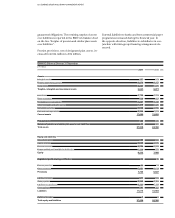

73 COMBINED GROUP AND COMPANY MANAGEMENT REPORT

Economic outlook for 2012

The global economy faces a number of major risks in

2012. Economic growth is generally expected to slow

down from approximately 3.0 % in 2011 to around 2.5 %

in 2012. The main influencing factors are likely to

remain the future course of the euro crisis on the one

hand and developments in the property and banking

sectors in China on the other.

Even if the euro crisis takes a positive course, the euro

zone economy is still predicted to stagnate as a whole.

Of all the major economies in the region, only Germany

is likely to achieve growth, albeit at a rate of only 0.2 %.

The other major countries are expected to see their

economic output drop: France by 0.5 %, Spain by 1.2 %

and Italy by 1.5 %. There is currently no end in sight to

the downward trend in Greece (– 5.0 %) and Portugal

(– 4.0 %). The UK economy is forecast to grow by 0.3 %.

By contrast, the recovery in the USA should continue

in 2012 and generate growth of approximately 1.8 %.

Although public-sector-spending austerity measures

will have the effect of holding down growth here, too,

there are nevertheless some signs of improvement on

the employment market and increases in consumer

spending.

The Japanese economy is forecast to grow in 2012 at a

rate of 2.5 %, helped by the backlog effect caused by lost

production after the natural desaster.

China is set to see growth slow down to 7.5 %, with ex-

ports held down by flagging demand from Europe, and

selling prices as well as revenue in the property sector

lower due to the restrictive monetary policies pursued

by the Chinese central bank.

A growth rate of 7.0 % is forecast for India. Given the size

of the country’s agricultural and consumer sectors, the

international weight of the Indian economy remains

limited. Lower raw materials prices are likely to dampen

growth in Brazil (+ 2.5 %) and Russia (+ 3.5 %).

Slightly weaker euro expected

The uncertainties prevailing within the euro zone sug-

gest that currency markets will again be highly volatile

in 2012. Given the expectation of a slight recovery of

the US economy and a weaker euro zone, the US dollar

may possibly gain in value slightly. The same applies

to the British pound and the Japanese yen. It is assumed

that the value of the Chinese renminbi will remain

coupled to the US dollar.

Car markets in 2012

The risks facing the global economy mean that the pros-

pects

for international car markets in 2012 are also

subject to uncertainty. The world’s largest car market,

China, is expected to grow by around 6 % to 18.5 million

units. Demand is expected to gain pace again in the

USA, with the car market expanding by around 6 % to

13.5 million units.

Due to economic uncertainties in the European Union,

the total number of cars sold in the region is forecast

to drop by 4 % to 12.5 million units. In Germany the

market is expected to consolidate at a level of 3.1 mil-

lion units. In France, we forecast that the market will

contract by approximately 6 % to 2.0 million. The British

market is likely to stagnate at just under 2.0 million

units. Further significant decreases are forecast in par-

ticular for both Italy and Spain. In Japan, the catch-up

effect after production losses in the past year could

well result in 20 % market growth to 4.8 million units.

Amongst the major emerging economies, the car

market in India is expected to register the highest

growth rate, whereas Brazil and Russia are only likely

to grow slowly.

Motorcycle markets in 2012

We do not expect to see any major recovery on inter-

national motorcycle markets in 2012. Given the uncer-

tain macroeconomic conditions, European markets are

unlikely to do more than move sideways. In the USA

and Japan, there is at least a chance that markets will

recover slightly. Another strong year is forecast for the

motor cycle market in Brazil.

The financial services market in 2012

The sovereign debt crisis is likely to be the dominant fac-

tor for financial services providers in 2012. Concerns

about the stability of the financial system could end up

being reflected in a high degree of volatility on

inter-

national financial markets.

Inflation is currently run-

ning at moderate levels. The expansionary monetary

policies being pursued by the major central banks

look set to continue for the time being. As long as

un-

certainty persists, volatile risk spreads are likely to

result in fluctuating refinancing costs for the whole

sector.

Selling prices on international used car markets should

remain generally stable in 2012. Price levels could,

however, fall in a small number of markets in southern

Europe in response to negative economic developments

and due to the fact that their used cars inventories are

Outlook