HSBC 2011 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

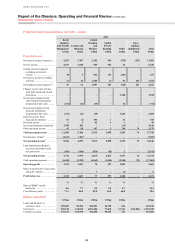

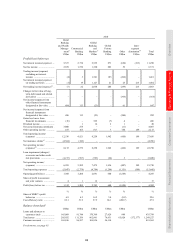

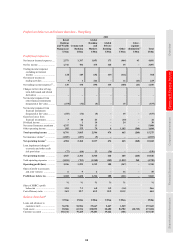

73

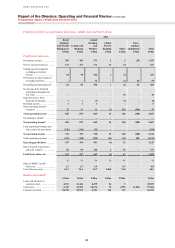

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

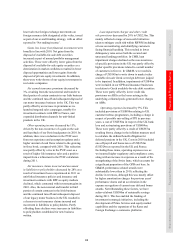

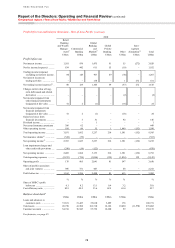

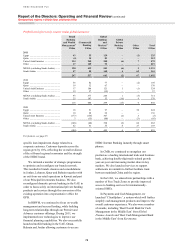

The growth in profitability in the region

reflected strong lending and deposit growth during

2010 and 2011, mainly in Singapore and mainland

China, coupled with widening deposit spreads due to

higher interest rates in certain countries, notably

India and mainland China. Loan impairment charges

improved as a result of the non-recurrence of a

number of individual impairments and the reduction

of certain unsecured lending portfolios. Costs

increased, though to a lesser extent than revenues, to

support business expansion, notably in mainland

China, and maintain our competitive position in our

six strategic markets. The contribution from our

associates in mainland China also grew, benefiting

from ongoing loan growth and increased income

from fee-based revenue streams.

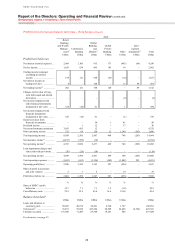

We continued to invest in building our franchise

in mainland China where the operating profit of our

operations more than doubled and we remained

the leading foreign bank by network size. In CMB,

we increased the coverage of our renminbi trade

settlement services to 24 cities within the country,

representing the widest geographic coverage among

all foreign banks, and offered renminbi capabilities

in over 50 countries worldwide. Cross-border

referrals between mainland China and the rest of the

world grew by 9% compared with 2010 as we

capitalised on our international network to capture

outbound and inbound trade flows. In GB&M, we

focused on leveraging our global connectivity and

product capabilities to be the leading international

bank of choice for multinational corporations doing

business with mainland China and large corporates

looking to expand internationally.

Profit before tax increased in other key countries

across the region as we maintained our strategic

focus on these markets, particularly in

intermediating cross-border trade flows. Trade

revenues grew in most of our sites and we were

awarded the ‘Best Trade Finance Bank in Asia

Pacific’ by FinanceAsia for the fourteenth

consecutive year. Trade-related lending grew

strongly in Singapore as we continued to enhance

our trade finance capabilities. In Malaysia we

expanded our branch network through the launch of

new Amanah branches. We also experienced strong

commercial lending growth in both Malaysia and

Indonesia as a result of various marketing

campaigns. In India, we were ranked the number one

foreign bank by Bloomberg for domestic bonds in

2011 and issued the first and only offshore renminbi

bond in the country.

As part of our strategic review process, in

December 2011 we announced the sale of our private

banking operations in Japan and, in January 2012,

we announced the sale of our RBWM operations in

Thailand. We expect to complete these transactions

during 2012.

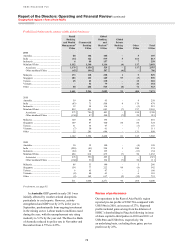

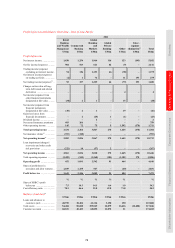

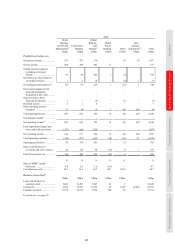

Net interest income increased by 28%. Average

lending balances grew most notably in CMB and

GB&M, particularly in mainland China, as we

captured inbound and outbound trade flows and as

demand for credit in the region increased. In RBWM

mortgage lending balances rose, notably in

Singapore and Australia, driven by competitive

product offerings and strong property markets.

This was partly offset by continued pressure on

asset spreads, most notably in RBWM (particularly

in Singapore and Australia), due to competitive

pressures and growth in residential mortgage lending

at lower spreads.

Customer deposit balances rose across most

of the region, notably in Payments and Cash

Management reflecting our investment in

infrastructure as part of a targeted strategy to

support growth in customer lending. Deposit spreads

increased as interest rates rose in a number of

countries, particularly in mainland China and India.

Net interest income from Balance Sheet

Management was higher than in 2010, reflecting

increased interest rates and the widening of onshore

US dollar lending spreads in mainland China, and a

higher return from short-term lending and growth in

the balance sheet in Singapore as we attracted

increased customer deposits.

Net fee income increased by 4%, primarily from

trade-related fees as we targeted asset growth and

trade activity, largely in mainland China, Bangladesh

and Singapore, supported by marketing activities,

customer acquisition and a rise in transactions from

existing customers. Card fees rose, notably in

Australia from the increased issuance of our co-

branded credit cards, higher retail spending, and

more customers converting to a higher card status.

Net trading income of US$1.7bn was broadly

unchanged compared with 2010. Net interest income

on trading activities was lower as we progressively

reduced our positions in government debt securities

following increased market volatility in bond

markets, and from growth in structured deposits

where the related income is recorded under ‘Net

interest income’. This was offset by higher Foreign

Exchange trading income due to increased customer

transaction volumes resulting from the collaboration

between GB&M and CMB and as more clients

sought protection from volatility in the markets.

Net expense from financial instruments

designated at fair value was US$18m compared with