HSBC 2011 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

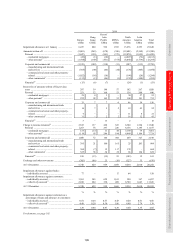

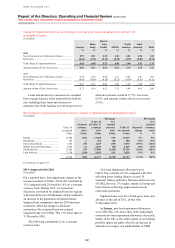

133

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

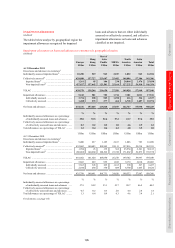

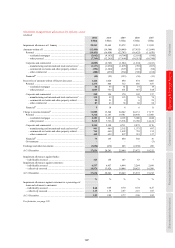

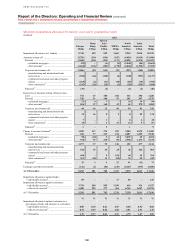

Corporate and Commercial forbearance

(Unaudited)

For the current policies and procedures

regarding forbearance in the corporate and

commercial sector, see the Appendix to Risk

on page 188.

The majority of the increase in renegotiated loans

activity for the commercial real estate sector in 2011

arose in Europe, which increased by US$617m. This

increase predominately related to the renegotiation

of a large exposure together with high levels of

forbearance in the UK towards the end of 2011

reflecting current economic conditions, including a

weakening in property values and a reduction in

institutions funding commercial real estate lending.

In the corporate and commercial sector the

increase in renegotiated loans in 2011 was again a

result of increased forbearance activity in Europe.

The increase related to renegotiations of a small

number of larger lending arrangements provided to

European corporate entities and economic pressures

in Europe more generally. This was partially offset

by repayments and write-offs of renegotiated loans

in Europe, Rest of Asia-Pacific and Latin America.

In the financial sector the increase in

renegotiated loans in 2011 primarily related to

financial difficulties in one financial sector entity. In

the government sector renegotiation activity was

wholly due to increases in Latin America caused by

term extension restructurings of municipal and local

authority facilities.

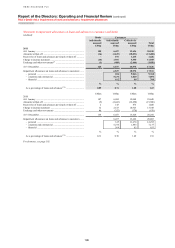

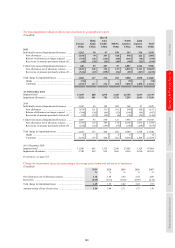

Impaired loans disclosure

(Audited)

During 2011 we adopted a revised disclosure

convention for the presentation of impaired loans

and advances which affects the disclosure of loans

and advances in the geographical regions with

significant levels of forbearance activity. The

previous impaired loan disclosure convention was

that impaired loans and advances were those

classified as CRR9, CRR10, EL9 or EL10 and all

retail loans 90 days or more past due, unless

individually they had been assessed as not impaired.

Renegotiated loans that did not meet the above

criteria were classified as ‘neither past due nor

impaired’ or ‘past due but not impaired’ as

appropriate, however these loans were assessed for

impairment in accordance with the Group’s

accounting policy on the recognition of impairment

allowances, as described on page 193.

The revised disclosure convention continues to

be based on internal credit rating grades and, for

retail exposures, 90 days or more past due status.

However, it introduces a more stringent approach to

the assessment of whether renegotiated loans are

presented as impaired. Management believes that

this revised approach better reflects the nature of

risks and inherent credit quality in our loan portfolio

as it is more closely calibrated to the types of

forbearance concession granted and applies stricter

requirements for the performance of renegotiated

loans before they may be presented as no longer

impaired. It also reflects developments in industry

best practice disclosure, as well as a refinement of

loan segmentation in our North America consumer

lending business. The revised disclosure convention

affects the disclosure presentation of impaired loans

but does not affect the accounting policy for the

recognition of impairment allowances.

Under this revised disclosure convention,

impaired loans and advances are those that meet any

of the following criteria:

• loans and advances classified as CRR 9, CRR

10, EL 9 or EL 10 (a description of our internal

credit rating grades is provided on page 191);

• retail exposures 90 days or more past due,

unless individually they have been assessed as

not impaired; or

• renegotiated loans and advances that have been

subject to a change in contractual cash flows as

a result of a concession which the lender would

not otherwise consider, and where it is probable

that without the concession the borrower would

be unable to meet its contractual payment

obligations in full, unless the concession is

insignificant and there are no other indicators

of impairment. Renegotiated loans remain

classified as impaired until there is sufficient

evidence to demonstrate a significant reduction

in the risk of non-payment of future cash flows,

and there are no other indicators of impairment.

For loans that are assessed for impairment on

a collective basis, the evidence to support

reclassification as no longer impaired typically

comprises a history of payment performance against

the original or revised terms, depending on the

nature and volume of forbearance and the credit risk

characteristics surrounding the renegotiation. For

loans that are assessed for impairment on an

individual basis, all available evidence is assessed on

a case by case basis.

In HSBC Finance, where a significant majority

of HSBC’s loan forbearance activity occurs, the

demonstrated history of payment performance is

with reference to the original terms of the contract,

reflecting the higher credit risk characteristics of this