HSBC 2011 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Risk > Credit risk > Credit exposure

106

European economic area, in particular by

transferring our excess liquidity away from

sovereign and bank-issued debt securities and from

money market placements with banks to placements

with central banks in the most highly-rated countries.

Despite this, we increased our overall exposure to

credit risk in 2011.

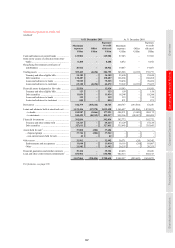

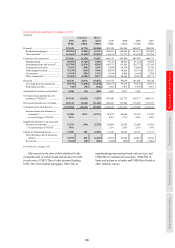

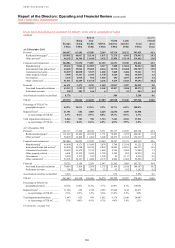

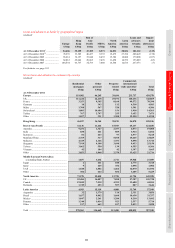

‘Maximum exposure to credit risk’ table (page 107)

The table presents our maximum exposure to credit risk from

balance sheet and off-balance sheet financial instruments

before taking account of any collateral held or other credit

enhancements (unless such enhancements meet accounting

offsetting requirements). For financial assets recognised on

the balance sheet, the maximum exposure to credit risk equals

their carrying amount; for financial guarantees and similar

contracts granted, it is the maximum amount that we would

have to pay if the guarantees were called upon. For loan

commitments and other credit-related commitments that are

irrevocable over the life of the respective facilities, it is

generally the full amount of the committed facilities.

Loans and advances to customers represent our

largest exposure to credit risk; however, this balance

reduced at the end of 2011, compared with the end

of 2010 as certain lending balances were reclassified

as ‘Assets held for sale’. We were able to

successfully grow our residential mortgage

portfolios in many other markets, notably in Hong

Kong and the UK where credit quality remained

high and LTV ratios were low.

Our exposure to loans and advances to banks

decreased in 2011, mainly in Europe as funds from

maturing term loans and reverse repo balances were

redeployed to ‘Cash and balances at central banks’.

This was offset in part by higher central bank

lending in Rest of Asia-Pacific, reflecting strong

deposit growth in the region. Our net exposure to

loans and advances to banks also decreased.

The loans and advances offset adjustment

primarily relates to customer loans and deposits

and balances arising from repo and reverse repo

transactions. The offset relates to balances where

there is a legally enforceable right of offset in the

event of counterparty default and where, as a result,

there is a net exposure for credit risk management

purposes. However, as there is no intention to settle

these balances on a net basis under normal

circumstances, they do not qualify for net

presentation for accounting purposes.

We increased our exposure to cash and balances

at central banks in 2011, as discussed above,

reflecting the placement of excess liquidity with

central banks in Europe and North America.

Our exposure to derivatives increased in 2011,

mainly in Europe reflecting an increase in the fair

value of interest rate contracts. This was

compounded by an increase in the notional value of

outstanding contracts, partly offset by higher netting

which rose in line with the increase in fair values.

Despite the increase in maximum exposure, our net

exposure to derivatives in 2011 decreased due to a

rise in the derivative offset.

The derivative offset amount in the table on

page 107 relates to exposures where the counterparty

has an offsetting derivative exposure with HSBC, a

master netting arrangement is in place and the credit

risk exposure is managed on a net basis or the

position is specifically collateralised, normally in the

form of cash. At 31 December 2011, the total amount

of such offsets was US$306bn (2010: US$198bn), of

which US$272bn (2010: US$178bn) were offsets

under a master netting arrangement, US$33.0bn

(2010: US$19.1bn) were collateral received in

cash and US$0.7bn (2010: US$0.2bn) were other

collateral. These amounts do not qualify for net

presentation for accounting purposes as settlement

may not actually be made on a net basis.

During 2011, we decreased our exposure to

trading assets. This reflected a reduction in our

holdings of government and highly-rated corporate

debt securities and equity positions, notably in

Europe. In addition, our reverse repo exposure

declined in North America as we did not replace

maturities.

In 2011, our loss experience continued to be

dominated by the personal lending portfolios, with

some 77% of our loan impairment charges related to

this lending category of which 56% was related to

US personal lending. This compared with 80% in

2010, of which 57% was related to US personal

lending.

While not considered as offset in the table

below, other arrangements including short positions

in securities and financial assets held as part of

linked insurance/investment contracts where the risk

is predominately borne by the policyholder, reduce

our maximum exposure to credit risk. In addition,

we hold collateral in respect of individual loans and

advances (see page 144).