HSBC 2011 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

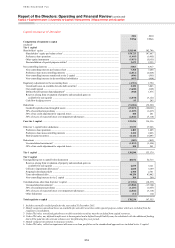

213

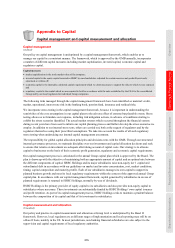

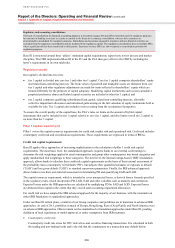

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

Regulation, removing national discretion, with the

exception of countercyclical and capital conservation

buffers which are in the Directive.

The Regulation additionally sets out provisions

to harmonise regulatory and financial reporting in

the EU. In December 2011, the EBA published a

consultative document proposing measures to

specify uniform formats, frequencies and dates

of prudential reporting to the regulator. The new

requirements are due to take effect as of 1 January

2013.

The CRD IV measures are subject to agreement

by the European Parliament, the Council and EU

member states.

In parallel with the Basel III proposals, the

Basel Committee issued a consultative document in

July 2011, Global systemically important banks:

assessment methodology and the additional loss

absorbency requirement. In November 2011, they

published their rules and the Financial Stability

Board (‘FSB’) issued the initial list of global

systematically important banks (‘G-SIBs’). This

list, which includes HSBC alongside twenty-eight

other major banks globally, will be re-assessed

periodically through annual re-scoring of the

individual banks and triennial review of the

methodology.

The rules set out an indicator-based approach to

G-SIBs assessment employing five broad categories:

size, interconnectedness, lack of substitutability,

cross-jurisdictional activity and complexity. The

designated G-SIBs will be required to hold minimum

additional common equity tier 1 capital of between

1% and 2.5%, depending on their relative systemic

importance indicated by their assessed score. A

further 1% charge may be applied to any bank

which fails to make progress, or even regresses, in

performance within the assessment categories. The

requirements, initially for those banks identified

in November 2014 as G-SIBs, will be phased in

from 1 January 2016, becoming fully effective on

1 January 2019. National regulators have discretion

to introduce higher thresholds than these minima.

The above forms part of a broad mandate of the

FSB to reduce the moral hazard of G-SIBs. A further

exercise of this mandate was the FSB’s own direct

consultation of October 2011. This proposed

introducing, over 2012-14, enhanced reporting

by G-SIBs to the Basel Committee centrally.

In September 2011, the ICB recommended

measures on capital requirements for UK banking

groups. For further details on these proposals see

page 101. The requirements as set out above indicate

the required regulatory common equity tier 1 ratio

for a G-SIB may ultimately lie in the range of 8% to

12%.

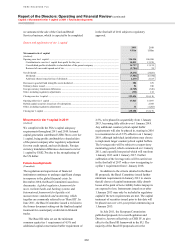

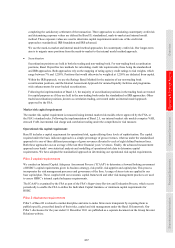

Potential common equity tier 1 requirements from

1 January 2019

(Unaudited)

Minimum common equity tier 1 4.5%

Capital conservation buffer 2.5%

Countercyclical capital buffer 0 – 2.5%

G-SIB buffer 1 – 2.5%

Against the backdrop of eurozone instability, on

a temporary basis, the EBA recommends banks aim

to reach a 9% core tier 1 ratio by the end of June

2012. We will continue to review our target core tier

1 ratio of 9.5% to 10.5% as the applicable regulatory

capital requirements evolve over the period to

1 January 2019.

Impact of Basel III

(Unaudited)

In order to provide some insight into the possible

effects of the Basel III rules on HSBC, we have

estimated the Group’s pro forma common equity

tier 1 ratio on the basis of our interpretation of those

rules applied to our position at 31 December 2011.

The Basel III changes will be progressively

phased in. The increased capital requirements which

come into effect on 1 January 2013 are estimated to

result in a common equity tier 1 ratio which is

100bps lower than the current core tier 1 ratio.

Management actions, primarily the run-off of legacy

positions including the US CML portfolio and the

sale of the US Card and Retail Services portfolio,

coupled with active management of the correlation

trading portfolio, the market risk capital requirement

and the counterparty capital risk requirement, will

mitigate this by 110bps, more than offsetting the

effect of these Basel III changes before taking

account of any future retained earnings.

In addition to the impact on common equity

tier 1 capital, tier 1 capital and tier 2 capital will also

be affected by the derecognition of non-qualifying

capital instruments. These changes will be phased in

over 10 years from 1 January 2013, and will further

reduce the tier 1 ratio by an estimated 10bps, and the

total capital ratio by an estimated 50bps in 2013,

excluding new issues of qualifying capital

instruments.

The changes to capital deductions and regulatory

adjustments including deferred tax assets, material

holdings, excess expected losses and unrealised

losses on available-for-sale portfolios will be phased

in over a five-year period starting on 1 January 2014.