HSBC 2011 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

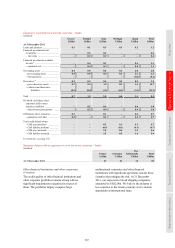

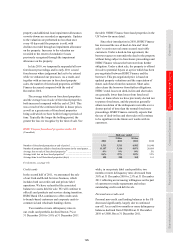

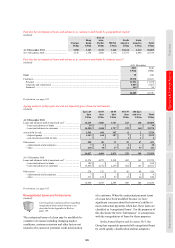

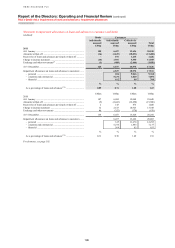

Risk > Credit risk > Areas of special interest > US personal lending // Credit quality of financial instruments

126

Two months and over contractual delinquency in the US

(Unaudited)

At 31 December

2011 2010 2009

US$m US$m US$m

In Personal Lending in the US

Residential mortgages ................................................................................................ 9,065 8,632 9,551

Of which:

Mortgage services .................................................................................................. 2,783 2,757 3,093

Consumer lending .................................................................................................. 5,139 4,861 5,380

Other mortgage lending .......................................................................................... 1,143 1,014 1,078

Second lien mortgage lending .................................................................................... 674 847 1,194

Of which:

Mortgage services .................................................................................................. 157 245 384

Consumer lending .................................................................................................. 344 423 642

Other mortgage lending .......................................................................................... 173 179 168

Vehicle finance ........................................................................................................... – – 267

Credit card .................................................................................................................. 714 957 1,798

Private label ................................................................................................................ 316 404 622

Personal non-credit card ............................................................................................. 513 811 1,548

Total ............................................................................................................................ 11,282 11,651 14,980

%

18 %

18 %18

Residential mortgages ................................................................................................ 17.1 15.0 14.5

Second lien mortgage lending .................................................................................... 8.5 9.1 10.1

Vehicle finance ........................................................................................................... – – 4.6

Credit card .................................................................................................................. 3.8 4.7 7.4

Private label ................................................................................................................ 2.5 3.0 4.1

Personal non-credit card ............................................................................................. 8.3 9.5 12.6

Total ............................................................................................................................ 11.4 10.7 11.1

For footnote, see page 185.

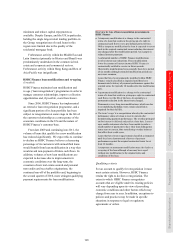

Credit quality of financial instruments

(Audited)

The five classifications describing the credit quality

of our lending, debt securities portfolios and

derivatives are defined in the Appendix to Risk on

page 188. Additional credit quality information in

respect of our consolidated holdings of ABSs is

provided on page 152.

During 2011, we amended our presentation of

impaired loans for portfolios with significant levels

of forbearance to provide more relevant information

on the effect of forbearance on the credit risk of

loans and advances. This change in presentation does

not affect the accounting policy for the recognition

of loan impairment allowances. Further details are

provided on page 133.

For the purpose of the following disclosure,

retail loans which are past due up to 89 days and are

not otherwise classified as impaired in accordance

with our disclosure convention (see page 133), are

not disclosed within the expected loss (‘EL’) grade

to which they relate, but are separately classified as

past due but not impaired.

2011 compared with 2010

We assess credit quality on all financial instruments

which are subject to credit risk, as shown in the

table on page 127. The balance of these financial

instruments was US$2,413bn, an increase of 5%

in 2011, of which US$1,649bn or 68% was classified

as strong. This percentage was broadly in line with

2010. The proportion of financial instruments

classified as good and satisfactory remained broadly

stable at 16% and 12%, respectively, while the

proportion of sub-standard financial instruments

was 2% in both 2011 and 2010.

Derivative assets increased by 33% to

US$346bn. This increase was mainly in Europe,

reflecting an increase in the fair value of interest rate

contracts compounded by an increase in the notional

value of outstanding contracts during the period. The

credit quality of our derivatives portfolio remained

strong with 81% of balances in this classification,

broadly in line with 2010.

Cash and balances at central banks, on which

credit quality has been assessed, more than doubled

to US$130bn. This increase was mainly in Europe

and in North America as we deposited a larger

portion of our excess liquidity with central banks in

these regions. As the increases in placements are