HSBC 2011 Annual Report Download - page 185

Download and view the complete annual report

Please find page 185 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

183

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

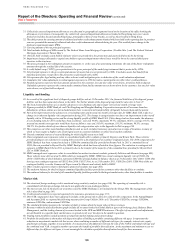

The cost of claims is a risk associated with non-

life insurance business. An increase in claims costs

would have a negative effect on profit. Our main

exposures to this scenario are in Hong Kong, Latin

America and Bermuda. Sensitivities have decreased

since 2010 due to the non-renewal and transfer to

third parties of certain contracts in our Irish business

as well as the disposal of the motor business in the

UK during 2011.

Mortality and morbidity risk is typically

associated with life insurance contracts. The effect

on profit of an increase in mortality or morbidity

depends on the type of business being written. Our

largest exposures to mortality and morbidity risk

exist in France, Hong Kong and the US.

Sensitivity to lapse rates depends on the type

of contracts being written. For insurance contracts,

claims are funded by premiums received and income

earned on the investment portfolio supporting the

liabilities. For a portfolio of term assurance, an

increase in lapse rates typically has a negative effect

on profit due to the loss of future premium income

on the lapsed policies. France, Hong Kong and the

UK are where we are most sensitive to a change in

lapse rates.

Expense rate risk is the exposure to a change in

expense rates. To the extent that increased expenses

cannot be passed on to policyholders, an increase in

expense rates will have a negative impact on our

profits.

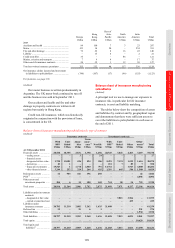

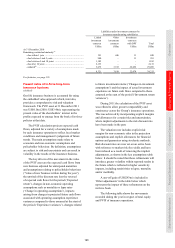

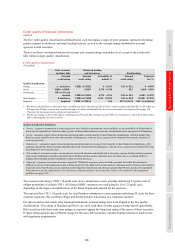

Sensitivity analysis

(Audited)

Effect on profit for the year

to 31 December

Effect on total equity

at 31 December

Life Non-life Total Life Non-life Total

US$m US$m US$m US$m US$m US$m

2011

20% increase in claims costs .............................. – (135) (135) – (135) (135)

20% decrease in claims costs ............................. – 135 135 – 135 135

10% increase in mortality and/or morbidity

rates ................................................................. (100) – (100) (100) – (100)

10% decrease in mortality and/or morbidity

rates ................................................................. 110 – 110 110 – 110

50% increase in lapse rates ................................. (349) – (349) (349) – (349)

50% decrease in lapse rates ................................ 609 – 609 609 – 609

10% increase in expense rates ............................ (89) (12) (101) (89) (12) (101)

10% decrease in expense rates ........................... 89 12 101 89 12 101

2010

20% increase in claims costs .............................. – (211) (211) – (211) (211)

20% decrease in claims costs ............................. – 211 211 – 211 211

10% increase in mortality and/or morbidity

rates ................................................................. (55) – (55) (55) – (55)

10% decrease in mortality and/or morbidity

rates ................................................................. 66 – 66 66 – 66

50% increase in lapse rates ................................. (203) – (203) (203) – (203)

50% decrease in lapse rates ................................ 363 – 363 363 – 363

10% increase in expense rates ............................ (63) (11) (74) (63) (11) (74)

10% decrease in expense rates ........................... 63 11 74 63 11 74

Other material risks

Reputational risk

(Unaudited)

The safeguarding of our reputation is

paramount. It is the responsibility of all

members of staff who are supported by

a global risk management structure

underpinned by relevant policies and

practices, readily available guidance, and

regular training.

As discussed in the Group Chief Executive’s

Business Review, we are placing a fresh emphasis

on values at HSBC, so that our employees are

empowered to do the right thing and to act with

courageous integrity. In 2011, we made HSBC

Values more explicit to ensure we meet the

expectations of society, customers, regulators and

investors. Those values are that we are dependable;

open to different ideas and cultures; and connected

to customers, communities, regulators and investors.

The Group acknowledges that it has not always

got this right in the past and that its conduct in

relation to the NHFA Limited, leading to the

imposition of a financial penalty, fell below the

standards we set for ourselves and required by

regulation. We recognise that our reputation was

damaged by this incident and we have committed