HSBC 2011 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

21

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

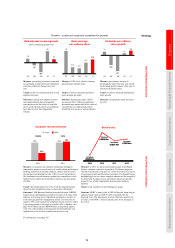

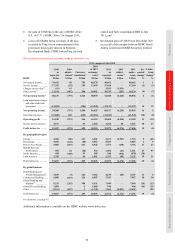

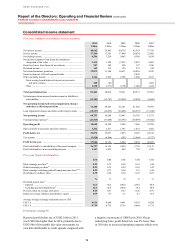

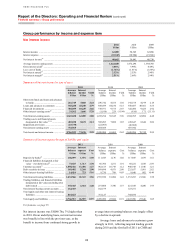

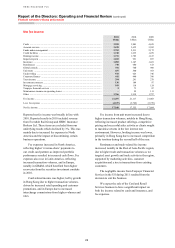

GB&M, as well as strong mortgage lending growth

in our RBWM businesses in the UK, Hong Kong and

Rest of Asia-Pacific throughout both years. During

the year, we announced the sale of 195 non-strategic

branches and our Cards and Retail Services business

in the US, and reclassified the related loans and

advances to customers to other assets held for sale,

reported within ‘Other interest-earning assets’. This,

together with the continued decline in the consumer

finance portfolios in run-off, partly offset the rise in

average lending balances in other regions.

The benefit to interest income of the strong

customer lending volume growth was offset in part

by a reduction in gross yields from loans and

advances to customers. This reflected the transfer of

balances to assets held for sale, including higher

yielding unsecured lending, the continued decline

within the US consumer finance portfolios and the

repositioning of RBWM towards higher quality

secured lending, particularly mortgages, together

with intense competition in certain markets.

Interest income from short-term funds and loans

and advances to banks also increased, attributable to

higher average balances with central banks. This

reflected higher deposit requirements by central

banks in certain markets, together with the placement

of excess liquidity in Asia with central banks.

Interest income from short-term funds and loans and

advances to banks, as well as financial investments,

also benefited from higher yields as interest rates

rose, particularly in mainland China, India and

Brazil.

Interest income from other interest earning

assets rose as a result of the reclassification of assets

held for sale and the related income.

The rise in interest income was largely offset

by higher interest expense. This was driven by a

significant increase in average customer account

balances in Hong Kong, Rest of Asia-Pacific and

Europe as a result of targeted deposit campaigns.

The cost of funds also rose as a result of base rate

increases, notably in mainland China, India and

Brazil, and competitive pricing to attract and retain

deposits in many markets.

The increase in interest expense on deposits

by banks was driven by a rise in the cost of funds in

Europe, reflecting the maturity of derivatives used to

hedge interest rate risk and their replacement at

lower prevailing interest rates.

The interest expense on own debt designated at

fair value also rose, reflecting the volume of new

issuances during the year. Although the average

balance of debt securities in issue declined due to

maturities not being replaced in North America and

Europe, the related interest expense increased as a

result of a general widening of credit spreads in the

financial sector.

‘Net interest income’ includes the expense of

internally funding trading assets, while related

revenue is reported in ‘Net trading income’. The

internal cost of funding these assets rose due to the

increase in average trading assets during the year. In

reporting our global business results, this cost is

included within ‘Net trading income’.

The decrease in the net interest spread compared

with 2010 was attributable to lower yields on loans

and advances to customers as we continued to target

higher quality assets, coupled with a rising cost of

funds on customer accounts. Our net interest margin

also fell, but by a lesser amount, due to the benefit

from net free funds. This benefit rose as a result of

the increase in the Group’s cost of funds, coupled

with higher third party funding of our trading book,

in line with the growth of trading assets.